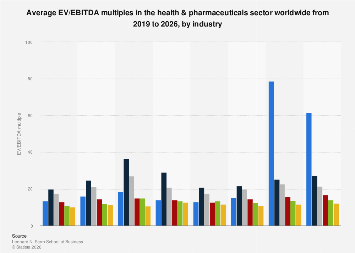

The global health and pharmaceuticals sector is poised to maintain robust valuation multiples, with the median Enterprise Value to Earnings Before Interest, Tax, Depreciation, and Amortization (EV/EBITDA) ratio projected to hover around a significant threshold in early 2026. This key financial metric, a widely used indicator of a company’s value relative to its operational profitability, suggests a continued investor confidence in the industry’s underlying strength and future growth prospects. The sector’s ability to consistently generate earnings, even amidst evolving market dynamics, underpins these favorable valuations.

Analysis of historical data, stretching from 2019 through to the projected figures for early 2026, reveals a sector that has navigated economic fluctuations and sector-specific challenges with notable resilience. While precise figures for the median EV/EBITDA remain proprietary and subject to subscription access, the overarching trend indicates a sustained appreciation, reflecting the indispensable nature of healthcare products and services. Furthermore, specific sub-segments within the broader health and pharmaceuticals landscape are exhibiting even higher valuation multiples. Companies operating within these particularly high-growth or high-margin niches are commanding average EV/EBITDA ratios that significantly exceed the sector-wide median, often surpassing the five-times mark. This disparity underscores the nuanced valuation landscape within the industry, where innovation, therapeutic area focus, and market leadership play pivotal roles in determining investor appetite.

The health and pharmaceuticals sector is characterized by several distinct industry segments, each with its own valuation drivers and market dynamics. These can range from large-cap pharmaceutical giants with diversified product portfolios and extensive research and development pipelines to specialized biotechnology firms focused on cutting-edge therapies, medical device manufacturers, and healthcare service providers. The EV/EBITDA metric, when applied across these diverse segments, provides a crucial benchmark for comparing the relative financial health and market perception of companies within the sector. For instance, companies engaged in the development of novel blockbuster drugs, particularly in areas with high unmet medical needs like oncology or rare diseases, often command premium valuations due to their potential for substantial future revenue streams and patent-protected market exclusivity.

The calculation of EV/EBITDA is a critical exercise for investors, analysts, and corporate strategists seeking to assess a company’s intrinsic value and its operational efficiency. Enterprise Value (EV) is calculated by adding the market capitalization of a company’s equity to its total debt, and then subtracting its cash and cash equivalents. This provides a comprehensive picture of the total capital invested in the business. EBITDA, on the other hand, represents a company’s operating performance before accounting for financing costs, taxes, and non-cash expenses such as depreciation and amortization. By dividing EV by EBITDA, analysts derive the EV/EBITDA multiple, which indicates how many years of earnings it would take for a company to pay back the market’s valuation of its business. A higher EV/EBITDA multiple generally suggests that investors expect higher earnings growth in the future, or that the company is perceived as having lower risk.

The figures used in these valuations are drawn from a comprehensive dataset encompassing a substantial number of companies within the health and pharmaceuticals sector. For the projected data pertaining to early 2026, the analysis includes approximately 4,504 companies. This sample size has progressively increased over the years, from 3,779 companies in 2019, indicating a growing breadth and depth of the data collection and analysis capabilities. This expansion in the number of companies analyzed strengthens the reliability and representativeness of the findings, offering a more granular view of the sector’s valuation trends. The consistency in including only companies with positive EBITDA further refines the analysis, ensuring that the multiples are derived from genuinely profitable operations.

The period from 2019 to 2025 has been a transformative one for the global economy and, by extension, the pharmaceutical industry. The COVID-19 pandemic, while presenting unprecedented challenges, also catalyzed significant advancements in drug discovery, vaccine development, and the adoption of digital health technologies. This era saw increased government spending on healthcare, heightened public awareness of medical research, and a renewed focus on supply chain resilience within the pharmaceutical sector. These factors have undoubtedly influenced the valuation multiples observed during this period, contributing to the sector’s overall resilience.

Looking ahead to 2025 and beyond, several key trends are expected to shape the valuation landscape of the health and pharmaceuticals sector. The ongoing pursuit of innovation remains paramount, with significant investment directed towards areas such as gene therapy, personalized medicine, and artificial intelligence-driven drug discovery. Companies that demonstrate a strong pipeline of innovative treatments and a clear path to market are likely to continue attracting premium valuations. Furthermore, the increasing focus on environmental, social, and governance (ESG) factors is becoming a more significant consideration for investors. Companies with strong ESG credentials, demonstrating a commitment to sustainability, ethical practices, and social responsibility, may see their valuations positively impacted.

The competitive landscape within the pharmaceutical industry is also evolving. Mergers and acquisitions (M&A) activity continues to be a strategic tool for companies seeking to expand their product portfolios, gain access to new technologies, or achieve economies of scale. Significant M&A deals can lead to substantial shifts in market share and influence the valuation multiples of both acquiring and target companies. Moreover, the growing importance of emerging markets as both sources of revenue and centers for research and development presents new opportunities and challenges for pharmaceutical companies, potentially influencing their global valuation strategies.

The regulatory environment also plays a critical role in shaping the fortunes of pharmaceutical companies. Changes in drug pricing regulations, patent laws, and approval processes in major markets such as the United States, Europe, and China can have a profound impact on a company’s profitability and, consequently, its valuation. Companies that can effectively navigate these complex regulatory frameworks and adapt to evolving policy landscapes are better positioned for sustained success.

In conclusion, the health and pharmaceuticals sector is projected to exhibit strong and stable valuation multiples in the near future, underpinned by its essential role in global health and its continuous drive for innovation. While the median EV/EBITDA provides a general indicator, the sub-sectoral variations highlight the importance of specific therapeutic areas, technological advancements, and market leadership in determining individual company valuations. As the industry continues to evolve, driven by scientific breakthroughs, shifting regulatory landscapes, and global economic forces, investors will likely maintain a keen interest in the sector’s ability to deliver both therapeutic value and financial returns. The sustained positive outlook for EV/EBITDA multiples serves as a testament to the sector’s enduring appeal and its critical contribution to human well-being and economic stability.