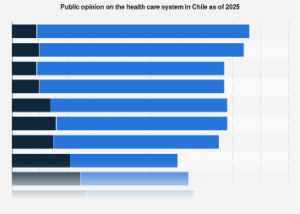

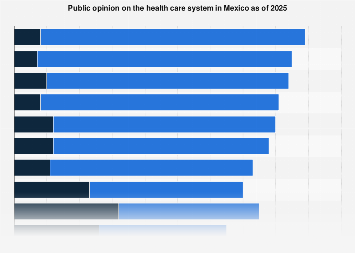

A significant portion of Mexico’s population harbors considerable skepticism regarding the nation’s healthcare system, with widespread concerns about affordability, accessibility, and the quality of care available. A comprehensive survey conducted in 2024 revealed that a mere fraction of respondents expressed confidence in their country’s ability to deliver optimal health treatments. This sentiment underscores a deep-seated apprehension that permeates public perception of healthcare provisions. Parallel to this lack of trust, a substantial majority of interviewees articulated a prevailing belief that a significant segment of the population struggles to afford quality healthcare, highlighting a critical socioeconomic barrier to well-being. Compounding these issues, a large percentage of individuals reported experiencing excessively long waiting times for medical appointments, suggesting systemic inefficiencies that impede timely access to essential services.

The landscape of healthcare coverage in Mexico is notably fragmented, with a substantial reliance on public health insurance programs. Data from a 2023 national survey indicates that over half of Mexican citizens benefit from public health insurance schemes that operate independently of social security institutions or private insurance providers. This signifies a crucial safety net for a large demographic, offering a baseline of medical support. Furthermore, the Mexican Social Security Institute (IMSS) plays a vital role, insuring a considerable proportion of the workforce and their dependents. Despite these public provisions, private health insurance remains a niche offering, covering a comparatively small percentage of the population. This disparity in coverage models highlights the dual nature of Mexico’s healthcare system, where public programs bear the brunt of responsibility for the majority, while private options cater to a more limited segment.

The issue of access to health services is far from uniform across Mexico, presenting a stark reality for over a third of the population. Even with the presence of social security and public healthcare initiatives, a significant number of Mexicans encounter substantial hurdles in obtaining necessary medical attention. In 2022, the proportion of individuals deemed vulnerable due to insufficient healthcare access saw a notable uptick, climbing from approximately 15% in 2016 to around 35% by 2022. This escalating vulnerability points towards systemic weaknesses that are exacerbating existing inequalities. The geographical distribution of these access disparities is particularly pronounced. For instance, the southern state of Chiapas exhibits the highest rate of healthcare vulnerability, with nearly 45% of its population facing significant challenges in accessing services. In stark contrast, Baja California Sur, located in the northwest, demonstrates the lowest vulnerability, with approximately 10% of its residents experiencing similar difficulties. This regional divergence underscores the uneven development of healthcare infrastructure and resource allocation across the country.

The economic implications of these healthcare challenges are far-reaching. A population that lacks confidence in its healthcare system, faces affordability issues, and experiences delayed access to care is likely to suffer from poorer health outcomes. This, in turn, can lead to decreased productivity, increased absenteeism from work, and a greater burden on public resources for managing chronic conditions and preventable illnesses. For individuals and families, the financial strain of seeking private medical care when public options are inadequate or inaccessible can be devastating, pushing many into poverty or debt. The disparities in access also translate into economic inequalities, as regions with poorer healthcare infrastructure may struggle to attract investment and retain skilled labor.

Globally, Mexico’s situation is not entirely unique, but the scale of its challenges warrants attention. Many developing nations grapple with similar issues of healthcare financing, infrastructure deficits, and equitable access. However, the pronounced regional disparities within Mexico, as highlighted by the contrast between states like Chiapas and Baja California Sur, suggest a need for targeted policy interventions and increased investment in underserved areas. International benchmarks often point to higher public health expenditure as a correlate of better health outcomes and greater public trust. While Mexico has made strides in expanding coverage through public programs, the qualitative aspects of care – such as waiting times and perceived quality – remain critical areas for improvement.

Looking ahead to 2025, the persistent concerns surrounding trust, affordability, and access are likely to remain central to the public discourse on healthcare in Mexico. Addressing these issues will require a multifaceted approach. This could involve strengthening the capacity of public health facilities, exploring innovative financing mechanisms to improve affordability, and implementing strategies to reduce waiting times and enhance the patient experience. Furthermore, investing in healthcare infrastructure and human resources in the most vulnerable regions will be crucial to bridging the access gap and ensuring that all Mexicans, regardless of their socioeconomic status or geographic location, can receive the quality healthcare they deserve. The economic prosperity and social well-being of the nation are intrinsically linked to the health of its citizens, making the reform and revitalization of its healthcare system a paramount national priority.