As the fiscal year draws to a close, a palpable urgency grips India’s industrial landscape, manifesting in a vigorous scramble for renewable energy certificates (RECs) and their international counterparts, I-RECs. This annual rush, driven by a complex interplay of governmental mandates and escalating corporate sustainability commitments, underscores a pivotal phase in the nation’s ambitious green energy transition. While demand surges, particularly from carbon-intensive sectors striving to meet compliance deadlines or internal environmental targets, the burgeoning supply of green power from India’s rapidly expanding renewable energy infrastructure has, for now, acted as a crucial dampener on price volatility, preventing a runaway spike in an otherwise highly active market.

The mechanism underpinning this market involves producers of clean electricity generating RECs for every megawatt-hour of renewable energy fed into the grid. These certificates are then unbundled from the physical electricity and become tradeable commodities. They serve as a crucial instrument for heavy emission industries and utilities to fulfill their Renewable Consumption Obligations (RCOs), which are statutory requirements set by the government to progressively increase the proportion of green energy in their total consumption mix. Simultaneously, a parallel market exists for International Renewable Energy Certificates (I-RECs), primarily sought by the Indian subsidiaries of multinational corporations from regions like North America, Europe, Japan, and South Korea. These entities often operate under global sustainability directives from their parent companies, aiming to achieve voluntary net-zero or renewable energy procurement targets that extend beyond local regulatory compliance.

The distinct nature of these certificates dictates their pricing and buyer profiles. Domestic RECs, issued and regulated by the National Load Despatch Centre (NLDC), are primarily acquired by state-owned power distribution companies (discoms) and large industrial power consumers. Their purchase is largely non-negotiable, driven by the imperative to avoid penalties for non-compliance with RCOs. In contrast, I-RECs are globally recognized instruments, and their procurement is typically a strategic decision aligned with a company’s broader Environmental, Social, and Governance (ESG) agenda. This distinction is reflected in their respective valuations and market dynamics. For instance, I-REC prices, while seeing an uptick towards the fiscal year-end, have risen from a low of ₹10-20 per megawatt-hour (MWh) to approximately ₹40-50, yet they remain below the ₹60-70 levels observed a year prior. Domestic RECs, being tied to mandatory obligations, have maintained a more stable pricing band, hovering around ₹350, despite robust demand.

This annual surge in demand is a predictable market phenomenon. "This increase happens generally at this time of year because corporates want to meet the 31 March target of sustainability," notes Aditya Malpani, a senior director and regional business development head at Ampin Energy Transition, a key player in renewable energy and I-REC trading. The financial year-end acts as a hard deadline, compelling companies to reconcile their renewable energy portfolios and acquire the necessary certificates to demonstrate compliance or progress towards their stated goals. This cyclical demand pattern highlights the dual pressures of regulatory enforcement and corporate accountability shaping India’s decarbonization efforts.

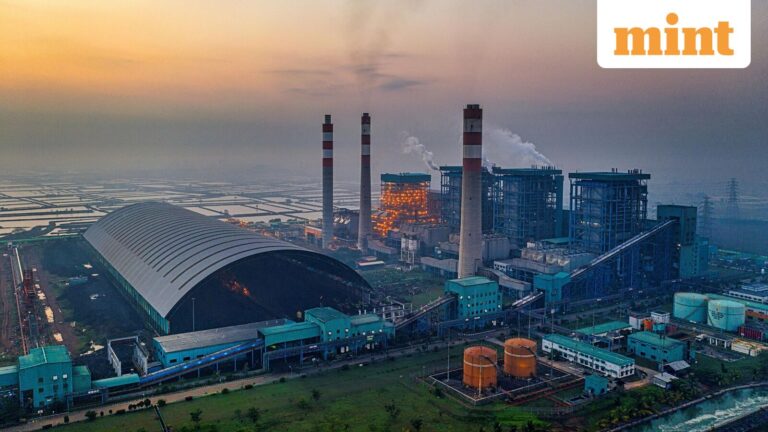

The rapid expansion of India’s renewable energy capacity over the past decade has fundamentally reshaped the supply side of this certificate market. From a modest 76 GW, constituting about a quarter of the nation’s total installed power generation capacity a decade ago, renewable energy capacity has now surpassed 180 GW, with ambitious national targets projecting over 250 GW by late 2025. This exponential growth, largely driven by significant government incentives, supportive policies, and private sector investment, has unleashed a considerable surplus of RECs and I-RECs. This abundant supply acts as a critical counterweight to the escalating demand, preventing the kind of acute price spikes seen in more constrained carbon markets globally.

Market data from platforms like the India Energy Exchange (IEX) vividly illustrates this supply-demand dynamic. In the previous year, the exchange recorded approximately 28 million buy bids for RECs against nearly 64 million sell bids, indicating a substantial overhang of supply. This imbalance is a primary reason why REC prices have remained relatively stable within a ₹325-370 range, even amidst intensified year-end purchasing activity. The availability of certificates ensures that entities facing compliance deadlines can generally acquire them without encountering prohibitive costs, thus supporting the viability of the RCO mechanism.

However, beneath the surface of overall market stability, specific sectoral challenges persist. Core industrial sectors, particularly those with high energy intensity such as chemicals, which account for over 50% of industrial power demand, have historically lagged in fulfilling their renewable power purchase obligations. "Core industrial sectors such as chemicals… have not really caught up on their renewable power purchase obligations. They have to now meet their obligations by purchasing RECs," stated Kartikeya Sharma, co-founder and chief business officer at independent power producer Sunsure, at a recent industry event. This deferred compliance often translates into a concentrated surge in demand for RECs as the fiscal year-end approaches, underscoring the necessity for robust enforcement mechanisms and proactive planning by these industries. The growing number of inquiries for RECs from these segments over the past two quarters suggests a belated but significant push towards compliance.

Looking ahead, the trajectory of India’s green certificate market will be influenced by several factors. The RCO targets are set to escalate significantly, demanding a substantial increase in renewable energy consumption from approximately 30% of total consumption in FY25 to a challenging 43.33% by FY30. This ambitious trajectory will undoubtedly sustain, if not intensify, demand for RECs. Concurrently, the global push for corporate net-zero targets and enhanced ESG reporting will continue to drive voluntary demand for I-RECs from multinational corporations operating within India.

From an economic perspective, the vibrant REC market serves multiple purposes. It provides an additional revenue stream for renewable energy generators, improving the financial viability of green power projects and incentivizing further investment in the sector. For industries, it offers a flexible mechanism to comply with environmental regulations without necessarily undertaking direct capital expenditure in renewable energy generation, though many are increasingly exploring hybrid models. This market mechanism, therefore, acts as a crucial enabler for India’s broader decarbonization agenda, facilitating the integration of renewables into the national energy mix and helping the country meet its international climate commitments.

The relatively low cost of RECs in India, compared to carbon credit prices in more mature markets like the European Union’s Emissions Trading System (EU ETS), reflects both the abundant supply and the specific regulatory framework. While this affordability aids compliance and encourages broader participation, it also raises questions about the long-term price signals required to drive truly transformative behavioral changes and significant new investments beyond mandated levels. As India progresses further in its energy transition, policy adjustments, potential market reforms, and the evolving global carbon pricing landscape will all play a role in shaping the future dynamics and efficacy of its green certificate market. For now, the delicate balance between surging demand and burgeoning supply ensures that India’s green transition, while dynamic, remains on a manageable and economically viable path.