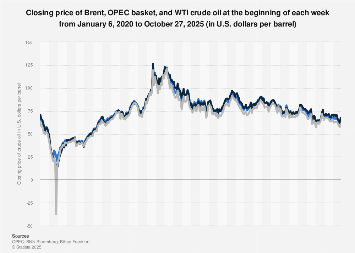

As of February 16, 2026, the benchmark for European crude oil, Brent, traded at $68.72 per barrel. This represented a modest uptick from the preceding week, with West Texas Intermediate (WTI), the primary U.S. benchmark, closing at $63.57, and the OPEC basket price at $66.81. These three reference points—Brent, WTI, and the OPEC basket—are critical indicators for global energy markets, influencing everything from gasoline prices at the pump to the economic health of nations heavily reliant on hydrocarbon exports.

The period between 2020 and 2026 has been marked by unprecedented volatility in the oil markets, underscoring the intricate interplay of global supply, demand, geopolitical events, and speculative trading. The year 2020, in particular, stands as a stark illustration of this sensitivity. The onset of the COVID-19 pandemic triggered a dramatic contraction in global oil demand. Lockdowns, widespread travel restrictions, and a general economic slowdown led to a precipitous drop in consumption, creating a surplus of crude oil that overwhelmed storage capacity. This demand shock was exacerbated by a geopolitical dispute between two of the world’s largest oil producers, Russia and Saudi Arabia, in early March 2020. Their initial disagreement over production cuts, followed by a tentative agreement on April 13th to reduce output, ultimately failed to immediately stabilize prices. The sheer volume of unsold oil, with storage facilities and even oil tankers rapidly filling up, led to a critical storage crunch. This culminated in a historic event between April 20th and April 22nd, 2020, where benchmark oil prices, specifically WTI futures, dipped into negative territory. This meant that sellers were effectively paying buyers to take the oil off their hands, a phenomenon driven by the urgent need to offload excess inventory before physical delivery obligations became unmanageable.

The fundamental drivers of crude oil prices are, as with most commodities, rooted in the classic economic principles of supply and demand. However, the oil market operates with unique complexities. A significant portion of crude oil is traded through futures contracts, which are agreements to buy or sell a commodity at a predetermined price on a future date. These contracts typically cover delivery within the next two to three months. This forward-looking nature means that market sentiment, investor speculation, and expectations about future production levels and consumer demand play an outsized role in price determination. Traders are constantly analyzing geopolitical developments, economic forecasts, technological advancements in extraction and alternative energy, and the potential impact of policy decisions by major oil-producing nations and consuming countries. Spot prices, on the other hand, reflect the immediate market value of a commodity for prompt delivery, offering a snapshot of current market conditions distinct from the longer-term outlook embedded in futures.

Looking at the data from January 2020 through February 2026, a clear pattern of extreme fluctuation emerges. The initial months of 2020 saw prices begin the year at relatively robust levels, with Brent trading above $68 per barrel and WTI around $63. The impact of the pandemic swiftly reversed this trend, pushing prices down dramatically. By April 2020, WTI futures infamously traded below zero, a stark anomaly. The subsequent recovery was gradual, influenced by the gradual easing of pandemic restrictions, the gradual restoration of economic activity, and continued efforts by OPEC+ (the Organization of the Petroleum Exporting Countries and its allies) to manage supply.

Throughout 2021 and into 2022, the oil market experienced a significant recovery. Global economic reopening spurred demand, while supply remained somewhat constrained due to underinvestment during the pandemic’s peak and ongoing production discipline from major players. Brent prices surged past $100 per barrel in early 2022, driven also by escalating geopolitical tensions, particularly the Russian invasion of Ukraine. This conflict disrupted global energy flows, fueled inflation, and prompted major consuming nations to release strategic petroleum reserves. The OPEC basket and WTI also mirrored this upward trajectory, reaching multi-year highs.

The latter half of 2022 and into 2023 saw a moderation in prices from their peaks, though still elevated compared to pre-pandemic levels. Concerns about a global economic slowdown, driven by aggressive interest rate hikes by central banks to combat inflation, began to weigh on demand expectations. Geopolitical factors, however, continued to inject volatility. For instance, Saudi Arabia and Russia, key players in OPEC+, have demonstrated a willingness to implement production cuts to support prices, often in response to perceived market imbalances or to counter the impact of rising non-OPEC supply, such as from the United States.

By early 2024, the oil market entered a phase of renewed upward momentum. Factors contributing to this included robust demand from emerging economies, particularly in Asia, and continued supply management by OPEC+. Geopolitical risks, including tensions in the Middle East and potential disruptions to shipping routes, added a premium to prices. Brent prices, for example, began to climb back towards the $80-$90 range, with WTI and the OPEC basket following suit. Projections for 2025 and early 2026 suggested a continued balancing act between robust demand, especially as economic growth stabilized in key regions, and the persistent influence of OPEC+ supply decisions and broader geopolitical stability. Forecasts from various energy agencies and financial institutions indicated a range of potential price points, often fluctuating between $70 and $90 per barrel for Brent, contingent on the evolving global economic landscape, the pace of the energy transition, and the geopolitical climate.

The economic implications of these price movements are profound. For oil-importing nations, sustained high oil prices translate to increased energy import bills, potentially widening trade deficits and contributing to inflationary pressures, which can dampen consumer spending and business investment. Conversely, oil-exporting countries can benefit from higher revenues, boosting their national budgets and economic growth. The global energy transition also plays a crucial role, with increasing investment in renewable energy sources and electric vehicles potentially dampening long-term oil demand, though the transition itself requires significant capital and is subject to various technological and policy hurdles. The strategic decisions of major oil producers, particularly within OPEC+, remain a dominant force in short-to-medium term price dynamics, making the ongoing monitoring of their production policies and geopolitical alignments essential for understanding the future trajectory of global energy markets. The data from 2020 to early 2026 clearly illustrates that oil prices are not merely a function of simple supply and demand but are deeply intertwined with global politics, economic sentiment, and the evolving landscape of energy consumption and production.