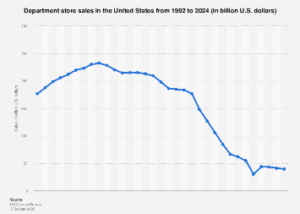

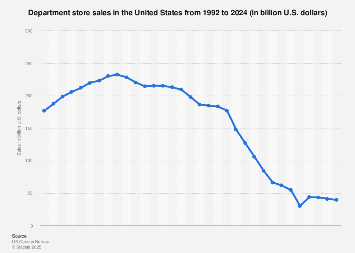

The U.S. department store sector in 2024 finds itself at a critical juncture, grappling with a complex interplay of evolving consumer preferences, intense online competition, and macroeconomic headwinds. While precise, up-to-the-minute sales figures for the entire sector often remain proprietary and require specialized market intelligence subscriptions, industry analysis and available data points indicate a period of significant recalibration. The traditional department store model, once a cornerstone of American retail, is undergoing a profound transformation as it seeks to redefine its relevance in an era dominated by e-commerce and direct-to-consumer brands.

For decades, department stores served as aspirational destinations, offering a curated selection of apparel, home goods, and cosmetics under one roof. However, the digital revolution has fundamentally altered how consumers shop. Online retailers, with their vast inventories, competitive pricing, and unparalleled convenience, have siphoned significant market share. This seismic shift has forced established players to confront declining foot traffic and a need to reinvent their value proposition. Companies like Macy’s, a prominent name in the sector, are actively engaged in strategic initiatives to adapt. Their efforts often involve optimizing store footprints, investing in digital capabilities, and experimenting with new store formats and experiential retail concepts.

The broader U.S. retail market, while showing resilience in certain segments, presents a challenging environment for legacy department stores. Inflationary pressures, while moderating, continue to influence consumer spending habits, leading to a greater emphasis on value and necessity. Discretionary spending, particularly on fashion and non-essential home goods, can be susceptible to economic uncertainty. This dynamic amplifies the pressure on department stores to offer compelling reasons for consumers to visit their physical locations or engage with their brands online. Statistics from market research firms often highlight a bifurcated retail landscape: strong performance in discount and off-price channels, alongside growth in specialized online retailers, leaving traditional mid-tier department stores in a precarious position.

Macy’s, for instance, has been a vocal proponent of its "A Bold New Chapter" strategy, which aims to revitalize the brand by focusing on owned brands, enhancing the digital customer experience, and optimizing its store portfolio. This includes strategic store closures of underperforming locations and investments in more profitable, higher-traffic flagships. The company’s financial performance, when analyzed, often reveals a narrative of navigating these transitional phases, with revenue streams being carefully managed and operational efficiencies being a constant pursuit. Key performance indicators such as same-store sales, online conversion rates, and inventory turnover become critical barometers of success in this environment.

Beyond individual company strategies, the economic impact on the department store sector is multifaceted. A struggling department store sector can have ripple effects on commercial real estate, employment, and associated industries like manufacturing and logistics. Conversely, a successful adaptation and resurgence could signal renewed consumer confidence and a healthy retail ecosystem. The employment figures associated with department stores, from sales associates to corporate staff, represent a significant segment of the retail workforce. Any significant contraction or expansion in the sector directly influences these numbers.

Global comparisons offer further context. In Europe, for example, department store chains have also faced similar challenges, with some adapting by focusing on luxury segments, embracing omnichannel strategies more aggressively, or transforming into curated marketplaces. In Asia, while e-commerce adoption is extremely high, certain department store formats have found success by integrating entertainment, dining, and personalized services, creating a destination experience rather than just a shopping venue. The U.S. market, with its vast geographic spread and diverse consumer base, presents unique challenges and opportunities that require tailored solutions.

Consumer behavior analysis is paramount to understanding the trajectory of department stores. Shoppers today are more informed, discerning, and digitally empowered than ever before. They research products online, compare prices across multiple platforms, and rely on peer reviews and social media influence. This necessitates that department stores not only offer desirable merchandise but also provide seamless, integrated shopping experiences that bridge the gap between online discovery and in-store fulfillment. Loyalty programs, personalized recommendations, and exceptional customer service are no longer differentiators but essential components of retaining customers.

The competitive landscape for department stores is incredibly crowded. They compete not only with other department stores but also with mass merchandisers, specialty retailers, online marketplaces like Amazon, and a growing number of direct-to-consumer brands that bypass traditional retail channels entirely. This intense competition forces department stores to continuously innovate and differentiate themselves. Investing in proprietary brands, developing exclusive collaborations, and creating unique in-store experiences are some of the strategies employed to capture consumer attention and loyalty.

Furthermore, the role of technology cannot be overstated. From sophisticated inventory management systems and data analytics to augmented reality try-on experiences and contactless payment options, technology is transforming the operational and customer-facing aspects of department stores. The ability to leverage data to understand customer preferences, personalize marketing efforts, and optimize supply chains is becoming a critical determinant of success. Those that fail to embrace these technological advancements risk being left behind.

In conclusion, the U.S. department store sector in 2024 is in a dynamic state of evolution. While facing considerable challenges from digital disruption and changing consumer habits, the sector is also demonstrating adaptability and innovation. The success of individual retailers will hinge on their ability to effectively integrate their physical and digital presences, offer compelling value propositions, and consistently meet the evolving expectations of the modern consumer. The coming years will likely see further strategic realignments, with a continued emphasis on customer-centricity and technological integration as key drivers of survival and growth in this highly competitive retail environment. The ongoing narrative is one of transformation, where resilience and strategic foresight will ultimately dictate the future of this enduring retail format.