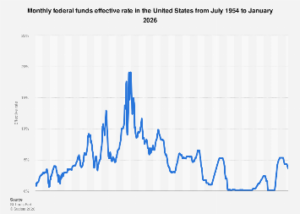

The Federal Reserve’s monetary policy entered a discernible easing cycle by 2026, marked by a series of downward adjustments to the federal funds effective rate. This strategic shift represented a significant departure from the preceding period of elevated rates. The year 2025 commenced with the federal funds rate standing at a particular percentage, following a rate cut implemented in January. This level was maintained until September 2025, when the Federal Open Market Committee (FOMC) opted to lower the rate to a different, more accommodative percentage. The easing trend gathered further momentum late in the year, with a reduction to yet another percentage in November, culminating in a final decrease to a new percentage by December. These successive cuts underscored a sustained commitment to a more expansionary monetary stance.

This pronounced phase of rate reductions followed an extended period where interest rates had been held at elevated levels, a situation that emerged in the wake of the unprecedented economic disruption caused by the COVID-19 pandemic. In the early months of 2020, the federal funds effective rate experienced a dramatic and swift decline. This aggressive move was a direct response to the severe economic shockwaves emanating from the pandemic. The rate plummeted from a February 2020 figure of X percent to Y percent by March, and by April, it had reached an historic low of Z percent. These emergency rate cuts, implemented in tandem with a large-scale quantitative easing program, were meticulously designed to inject liquidity into financial markets, stabilize economic activity, and prevent a more profound economic contraction. The benchmark rate remained anchored near zero for nearly two years, a period of sustained accommodative policy.

The economic landscape began to shift in early 2022, prompting the Federal Reserve to initiate a significant tightening cycle. This marked a reversal of the pandemic-era stimulus. The federal funds rate began its ascent, moving from a rate of A percent in April 2022 to a peak of B percent by August 2023. This period of rate hikes aimed to combat burgeoning inflationary pressures that had become a growing concern. After maintaining this restrictive stance for over a year, allowing the effects of tighter monetary policy to permeate the economy, the Federal Reserve signaled a change in its policy direction. This pivot commenced in September 2024 with a reduction in the federal funds rate to C percent, followed by a further cut to D percent in December 2024. These actions in the latter half of 2024 effectively signaled the beginning of a broader policy recalibration, a trend that would continue and intensify throughout 2025 and into 2026.

The federal funds effective rate serves as a pivotal benchmark in the U.S. financial system. It represents the interest rate at which depository institutions, such as commercial banks and credit unions, lend their reserve balances to other depository institutions on an overnight basis. This interbank lending rate is a critical tool for monetary policy, and adjustments to it have a profound and wide-ranging impact across the entire economy. Changes in the federal funds rate influence borrowing costs for businesses and consumers, affecting investment decisions, consumption patterns, and ultimately, the pace of economic growth. Furthermore, it plays a crucial role in managing inflation by influencing the cost of credit and the overall level of demand in the economy.

The trajectory of interest rate adjustments undertaken by the Federal Reserve in the post-pandemic era can be viewed within a broader context of global central bank policy responses. In the initial phase of the COVID-19 crisis in early 2020, a near-universal adoption of aggressive monetary easing measures was observed among central banks worldwide. This synchronized global response was aimed at cushioning the economic blow of widespread lockdowns and supply chain disruptions. The Federal Reserve’s swift reduction of the federal funds rate from E percent in February to F percent by April 2020 was largely in step with actions taken by its international counterparts. For instance, the European Central Bank (ECB) and the Bank of England (BoE) also implemented significant stimulus measures to support their respective economies.

This period of ultra-low interest rates persisted through 2021, providing a stable backdrop for economic recovery. However, by 2022, a significant surge in inflation, driven by a confluence of factors including supply chain bottlenecks, strong consumer demand fueled by pent-up savings, and geopolitical events, necessitated a change in course. This led to a synchronized global tightening cycle, with major central banks, including the Federal Reserve, the ECB, and the BoE, embarking on a series of interest rate hikes to bring inflation back under control. This concerted effort to combat inflation was a testament to the shared understanding of the risks posed by sustained price pressures.

As inflation began to moderate from its peaks in mid-2024, a gradual shift back towards accommodative monetary policy became evident among many central banks. The Federal Reserve’s decision to cut rates in late 2024 and continue this trend through 2025 and into 2026 was mirrored by similar easing actions in other advanced and emerging economies. This global pivot towards lower interest rates reflects a delicate balancing act by policymakers, aiming to foster economic growth and employment without reigniting inflationary pressures. The effectiveness of these policy adjustments will be closely monitored by global markets, as they navigate the evolving economic landscape. The sustained reduction in the federal funds rate through 2026 signifies the Fed’s strategic recalibration, moving from an era of aggressive tightening to one of deliberate easing, in response to shifting economic conditions and evolving inflation dynamics. This protracted easing cycle is expected to influence borrowing costs, investment strategies, and overall economic activity across the United States and its trading partners.