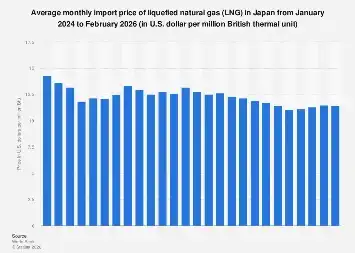

Japan, a nation heavily reliant on imported energy, has historically navigated the volatile global liquefied natural gas (LNG) market with a keen eye on pricing dynamics. The average monthly import price per million British thermal units (MMBtu) serves as a critical barometer for the nation’s energy security, economic stability, and its broader industrial competitiveness. Fluctuations in this key metric are not merely statistical anomalies; they represent significant shifts in geopolitical influence, supply chain resilience, and the ongoing global transition towards cleaner energy sources. Understanding these price movements is paramount for policymakers, energy corporations, and the Japanese public alike.

For decades, Japan has been the world’s largest importer of LNG, a position cemented by its lack of domestic fossil fuel reserves and its post-war industrial boom. This dependence, however, has always come with inherent vulnerabilities, particularly concerning price volatility. The cost of LNG is influenced by a complex interplay of factors, including global supply and demand, geopolitical events, weather patterns, shipping costs, and the pricing mechanisms of long-term contracts versus the spot market. The MMBtu price, a standard unit of energy measurement, allows for consistent comparison across different types of fuels and international markets, making it an indispensable tool for analyzing Japan’s energy expenditure.

Recent trends have highlighted the increasing complexity of this market. While historically Japan benefited from long-term contracts often indexed to oil prices, the global energy landscape has evolved dramatically. The rise of new LNG producers, particularly in the United States and Australia, has increased supply diversity. Simultaneously, a surge in demand from emerging economies, coupled with unexpected disruptions such as extreme weather events or geopolitical tensions, has led to significant price spikes. The aftermath of the war in Ukraine, for instance, sent shockwaves through global energy markets, with European nations scrambling for alternative supplies and bidding up prices, inevitably impacting Asian markets where Japan is a dominant buyer.

The MMBtu price for Japanese LNG imports is not a static figure; it is a dynamic indicator reflecting the real-time pressures on the global energy trade. When this average price rises, it directly translates into higher electricity and gas bills for Japanese households and businesses. For industries that are energy-intensive, such as petrochemicals, steel, and manufacturing, increased energy costs can erode profit margins, potentially leading to reduced output, a slowdown in investment, and a diminished capacity to compete internationally. This ripple effect underscores the profound economic implications of LNG import prices.

Furthermore, the cost of LNG directly impacts Japan’s trade balance. As a major importer, a sustained increase in LNG prices can widen the country’s trade deficit, putting pressure on the Japanese Yen and potentially influencing broader macroeconomic policies. The Ministry of Economy, Trade and Industry (METI) and other governmental bodies continuously monitor these figures to formulate energy policies, negotiate import agreements, and strategize for future energy procurement.

The global comparison of LNG prices offers valuable context. While Japan has historically been a price-setter in the Asian market, the emergence of new buyers and the increasing influence of the spot market have altered this dynamic. Nations in South Asia, such as Pakistan and Bangladesh, are also becoming increasingly significant LNG importers, often competing for cargoes and contributing to price pressures. European countries, driven by a desire to reduce reliance on Russian gas, have also been aggressively seeking LNG supplies, at times outbidding Asian buyers for available spot cargoes. This heightened competition means that the MMBtu price in Japan is increasingly influenced by factors far beyond its immediate supply and demand dynamics.

Experts in the energy sector emphasize that Japan’s strategy to mitigate price volatility involves a multi-pronged approach. This includes diversifying its LNG supply sources, exploring new export regions, and investing in flexible contracts that offer some degree of price hedging. The development of domestic renewable energy sources, such as solar and wind power, and the potential re-activation of nuclear power plants are also crucial components of Japan’s long-term energy security strategy, aimed at reducing its overall dependence on imported fossil fuels, including LNG.

Statistics on average monthly LNG import prices per MMBtu for Japan, while often proprietary and requiring subscription for detailed access, are meticulously tracked and analyzed. These datasets typically reveal significant seasonal variations, with prices often peaking during the winter months when heating demand increases in the Northern Hemisphere. However, the unprecedented price surges seen in recent years have demonstrated that seasonal factors are now frequently overshadowed by larger geopolitical and supply-side disruptions.

The economic impact analysis of these price trends is multifaceted. For instance, a study might examine how a 10% increase in the average MMBtu price impacts the operating costs of the Japanese chemical industry, or how it affects the disposable income of households, thereby influencing consumer spending patterns. Such analyses are critical for government planning and for guiding private sector investment decisions in the energy-intensive sectors.

Moreover, the evolution of LNG pricing itself is a subject of ongoing debate. The traditional oil-indexed pricing mechanisms, which provided some price stability for Japan over the long term, are gradually being supplemented or replaced by alternative models, including Henry Hub (US natural gas benchmark) indexation and even direct spot market pricing. This shift introduces new forms of price risk and reward, requiring sophisticated risk management strategies from Japanese energy importers.

The future trajectory of Japan’s LNG import prices will likely be shaped by several key developments. The global energy transition, with its emphasis on decarbonization, will continue to influence investment in new LNG export infrastructure. The development of new technologies, such as floating liquefied natural gas (FLNG) facilities, could also alter supply dynamics. Furthermore, the ongoing efforts by major economies to secure long-term energy supplies amidst geopolitical uncertainties will continue to create a competitive and often unpredictable market. For Japan, maintaining energy security while managing costs in this evolving landscape remains a paramount economic and strategic imperative. The average monthly LNG import price per MMBtu is, and will continue to be, a vital indicator of its success in this endeavor.