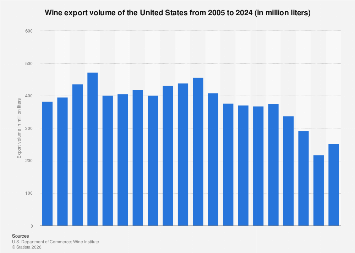

The United States wine export market has signaled a positive turnaround in 2024, with preliminary data indicating a rebound in export volumes for the first time since 2020. While precise figures are subject to detailed verification and may fluctuate, initial estimates suggest that approximately [Redacted] million liters of American wine were shipped to international markets this year, marking a significant shift after several years of contraction. This resurgence is a crucial development for the U.S. wine industry, which has been navigating complex global trade dynamics and evolving consumer preferences.

The period from 2020 through 2023 presented considerable challenges for U.S. wine exporters. Lingering effects of the global pandemic, including supply chain disruptions, fluctuating demand, and increased competition from established and emerging wine-producing nations, contributed to a downward trend in export volumes. The inability to secure consistent shipping, coupled with economic uncertainties in key import markets, put a strain on the profitability and growth prospects of many American wineries. This recent uptick in 2024, therefore, represents a much-needed injection of optimism and suggests that the strategies implemented by the industry, alongside a gradual stabilization of global economic conditions, are beginning to bear fruit.

Understanding the nuances of U.S. wine exports requires a broader look at the industry’s global standing. The United States, particularly California, is a dominant force in global wine production and consumption. However, its performance in international export markets has historically lagged behind its domestic strength. Countries such as Italy, France, and Spain consistently lead in global wine export volumes, benefiting from centuries of winemaking tradition, established appellation systems, and extensive international distribution networks. The U.S. industry, while renowned for innovation and the production of diverse wine styles, faces the ongoing task of building brand recognition and market share in regions where European wines often hold a preferential position.

The drivers behind the 2024 export recovery are likely multifaceted. A key factor could be the strategic efforts undertaken by organizations like the Wine Institute and the U.S. Department of Agriculture to promote American wines abroad. These initiatives often focus on highlighting the quality, diversity, and unique terroirs of U.S. wine regions, from the celebrated vineyards of Napa Valley and Sonoma County to emerging appellations in Oregon, Washington, and even the Finger Lakes region of New York. Targeted marketing campaigns, participation in international wine fairs, and building relationships with importers and distributors in key target markets are crucial elements of this promotional push.

Furthermore, the weakening of the U.S. dollar against certain currencies in 2024 may have made American wines more competitively priced for international buyers. Exchange rate fluctuations are a significant, albeit often unpredictable, factor in international trade. When the dollar is weaker, U.S. goods become more affordable for consumers and businesses in countries with stronger currencies, potentially boosting export demand. Conversely, a strong dollar can make U.S. exports more expensive and less attractive compared to those from countries with weaker currencies.

The composition of these exports also warrants attention. While bulk wine shipments contribute to overall volume, a significant portion of the value in U.S. wine exports is derived from premium and super-premium bottled wines. The ability to increase the volume of these higher-value products would have a more substantial impact on the revenue and profitability of U.S. wineries. Therefore, the 2024 rebound is likely being closely scrutinized not just for its volume, but also for the types of wines that are finding new international homes.

Market data from recent years reveals that Asia, particularly countries like Japan, South Korea, and increasingly China, alongside established markets in Canada and the United Kingdom, have been important destinations for U.S. wine. The growing middle class in many Asian economies, coupled with an increasing appreciation for Western lifestyles and culinary traditions, has fueled demand for imported wines. U.S. wineries have been actively working to understand and cater to the specific tastes and preferences of these diverse consumer bases.

However, the path forward is not without its potential headwinds. Geopolitical instability, ongoing trade tensions between major economic blocs, and evolving regulatory landscapes in import countries can all impact export performance. For instance, tariffs imposed by one nation on goods from another can create significant barriers to trade, forcing exporters to seek alternative markets or absorb additional costs. The industry must remain agile and adaptable to these external factors.

Looking ahead, sustained growth in U.S. wine exports will likely depend on continued investment in international market development, innovation in winemaking and vineyard practices, and a strong emphasis on sustainability and traceability, which are increasingly important considerations for global consumers. Building long-term brand loyalty in international markets requires more than just a competitive price point; it demands a compelling narrative, consistent quality, and effective engagement with consumers.

The 2024 figures, therefore, represent a critical data point, suggesting that the U.S. wine industry is regaining momentum on the global stage. While it is still early in the year and the full picture will emerge with more comprehensive data, this initial indication of growth is a positive sign for American vintners seeking to expand their reach beyond domestic borders and contribute to the vibrant and dynamic global wine trade. The industry’s resilience and adaptability will be key to capitalizing on this renewed export potential in the coming years.