The global chemical industry, a bedrock of modern economies, is undergoing a significant transformation, with Asia-Pacific solidifying its position as the dominant force in revenue generation. This sprawling sector, encompassing everything from basic petrochemicals and polymers to specialty chemicals and advanced materials, is not a monolithic entity but rather a complex mosaic of regional strengths, technological advancements, and evolving market demands. Understanding the revenue share by region is crucial for grasping the current landscape and forecasting future investment and innovation trajectories.

For years, Asia-Pacific has been the undisputed leader, driven by robust economic growth, burgeoning industrialization, and a vast consumer base across countries like China, India, and Southeast Asian nations. China, in particular, has emerged as the world’s largest chemical producer and consumer, accounting for a substantial portion of global output. This dominance is fueled by a combination of factors: significant domestic demand from downstream industries such as automotive, construction, and electronics; government support for the sector; and a well-established manufacturing infrastructure. The sheer scale of production in China often influences global pricing and supply chains for a wide array of chemical products.

Beyond China, other Asian economies are also playing increasingly important roles. India’s chemical industry is experiencing rapid growth, supported by government initiatives like "Make in India" and a growing focus on specialty chemicals. South Korea and Japan, while mature markets, remain at the forefront of innovation, particularly in high-value specialty chemicals and advanced materials, often serving as crucial suppliers of sophisticated components to global electronics and automotive sectors. The Association of Southeast Asian Nations (ASEAN) bloc, with countries like Singapore, Thailand, and Malaysia, also contributes significantly, benefiting from strategic geographic locations and increasing foreign investment.

In contrast, Europe, historically a powerhouse in the chemical sector, particularly in Germany, is navigating a period of strategic recalibration. While still a significant player, especially in specialty chemicals, pharmaceuticals, and sustainable solutions, the region faces challenges related to energy costs, stringent environmental regulations, and increasing competition from Asia. European chemical giants are increasingly focusing on higher-margin, research-intensive products and investing in green chemistry and circular economy initiatives to maintain their competitive edge. The emphasis is shifting from bulk commodity production to value-added solutions and sustainable alternatives, reflecting a broader global trend towards environmental responsibility.

North America, led by the United States, remains a vital hub for the chemical industry, benefiting from abundant and relatively inexpensive feedstock, particularly natural gas, which provides a competitive advantage for petrochemical production. The shale gas revolution has revitalized the U.S. chemical manufacturing sector, leading to significant investments in new capacity and expansion projects. The U.S. is also a leader in innovation, particularly in advanced materials, agricultural chemicals, and specialty polymers. However, like Europe, the region is also grappling with the need to decarbonize its operations and develop more sustainable chemical processes.

The Middle East, leveraging its vast oil and gas reserves, continues to be a major producer of basic petrochemicals and polymers. Countries like Saudi Arabia, Qatar, and the UAE have strategically invested in large-scale, integrated chemical complexes, capitalizing on their feedstock advantage to supply global markets. While primarily focused on commodity chemicals, there is a growing trend towards diversification into downstream products and specialty chemicals to capture more value. The region’s role as a major exporter of these materials makes it a critical link in the global chemical supply chain.

Latin America’s chemical industry, while not matching the scale of other major regions, possesses significant potential. Brazil, as the region’s largest economy, is a key player, with a diverse chemical sector serving its agricultural, industrial, and consumer markets. Argentina and Mexico also contribute to the regional output. Challenges in Latin America often relate to infrastructure, political stability, and access to capital, but opportunities exist in areas like agrochemicals, biofuels, and specialty chemicals catering to local and regional demand.

The revenue share dynamics are not static; they are constantly influenced by macroeconomic trends, geopolitical events, technological breakthroughs, and evolving consumer preferences. For instance, the global push towards electrification and renewable energy is creating new demands for advanced materials used in batteries, solar panels, and wind turbines, areas where innovation is key. Similarly, the growing emphasis on sustainability and circular economy principles is driving investment in bio-based chemicals, recycled plastics, and more efficient manufacturing processes.

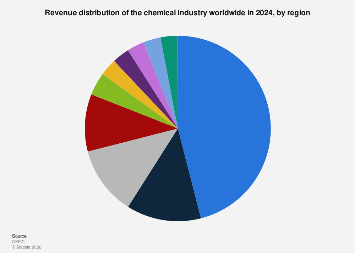

Statistics from market intelligence firms consistently highlight the leading position of Asia-Pacific, often accounting for well over half of the global chemical market revenue. This dominance is not solely about volume but also increasingly about value as Asian companies move up the value chain into more sophisticated products. For example, in 2023, estimates suggested that Asia-Pacific’s share of the global chemical market revenue could exceed 55%, with China alone representing a significant chunk of that. Europe typically follows, with a share in the mid-to-high teens, while North America occupies a similar bracket. The Middle East and Latin America represent smaller but significant portions of the global revenue pie.

These regional disparities have profound implications for global trade flows, investment decisions, and research and development priorities. Companies operating in the chemical sector must maintain a keen understanding of these regional dynamics to effectively navigate the market, identify growth opportunities, and mitigate risks. The future of the global chemical industry will likely be shaped by a continued emphasis on sustainability, digital transformation, and the ability of regions to adapt to shifting economic and environmental landscapes, with Asia-Pacific poised to remain at the forefront of this evolution.