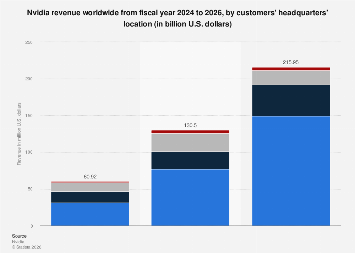

Nvidia’s projected revenue distribution by the headquarters of its clientele in fiscal year 2026 is poised to underscore the company’s pivotal role in the global artificial intelligence and high-performance computing landscape. While precise, granular data for this forward-looking period often resides behind premium access tiers for market intelligence firms, broader industry trends and Nvidia’s strategic positioning offer substantial insights into its anticipated revenue streams. The company’s dominance in AI accelerators, particularly its Graphics Processing Units (GPUs), has made it an indispensable partner for a wide array of industries, from cloud computing giants and enterprise data centers to automotive manufacturers and scientific research institutions.

The United States, as the epicenter of technological innovation and home to many of the world’s largest technology companies, is expected to remain Nvidia’s largest revenue contributor. This is driven by the substantial investments these U.S.-based entities are making in AI infrastructure. Leading cloud service providers, such as Amazon Web Services, Microsoft Azure, and Google Cloud, are engaged in an unprecedented build-out of their AI capabilities, requiring vast quantities of Nvidia’s cutting-edge GPUs to power their services, train complex AI models, and deploy AI-driven applications for their global customer bases. The insatiable demand for data processing and model training, fueled by generative AI, large language models, and advanced analytics, directly translates into significant revenue for Nvidia from these U.S. headquarters.

Beyond the hyperscalers, U.S. enterprises across various sectors, including finance, healthcare, and entertainment, are increasingly integrating AI into their operations. This encompasses everything from fraud detection and personalized medicine to content creation and recommendation engines. The research and development arms of major U.S. corporations, heavily invested in pushing the boundaries of AI, also represent a significant market segment for Nvidia’s specialized hardware. The company’s ability to consistently deliver performance improvements and cater to the evolving demands of these sophisticated customers solidifies the U.S.’s position as a cornerstone of Nvidia’s financial performance.

The Asia-Pacific region, with a strong emphasis on East Asia, is another critical geography for Nvidia’s revenue. While China’s domestic semiconductor industry is actively developing its own AI chip capabilities, the sheer scale of demand for advanced computing power, particularly from Chinese technology giants and burgeoning AI startups, ensures a substantial market for Nvidia’s products. Companies like Baidu, Alibaba, and Tencent, major players in cloud computing, e-commerce, and social media, are significant consumers of Nvidia’s GPUs for their extensive AI research and deployment efforts. The rapid digitalization of the Chinese economy and the government’s strategic focus on AI development further amplify this demand.

However, geopolitical considerations and evolving export controls, particularly concerning advanced AI chips to China, introduce a layer of complexity and potential flux in this revenue stream. While Nvidia has historically been a dominant supplier, regulatory shifts could impact the types and quantities of chips that can be exported, potentially influencing revenue figures. Despite these challenges, the fundamental need for high-performance AI processing within China’s massive digital economy remains, and Nvidia continues to adapt its product offerings and strategies to navigate this intricate market.

Taiwan and South Korea, also key components of the Asia-Pacific market, contribute significantly through their leading semiconductor manufacturing and consumer electronics companies. Taiwan Semiconductor Manufacturing Company (TSMC), Nvidia’s primary foundry partner, not only manufactures Nvidia’s chips but also benefits from the immense demand that Nvidia generates. Furthermore, South Korean conglomerates, such as Samsung and SK Hynix, are major players in areas like memory and advanced packaging, crucial elements in the AI hardware ecosystem. Their own AI initiatives and the demand for high-performance computing in their respective markets also represent important revenue avenues for Nvidia, either directly through hardware sales or indirectly through their integration into broader technology solutions.

Europe, while perhaps not matching the scale of North American or East Asian demand on a single-company basis, presents a diversified and growing market for Nvidia. The continent is experiencing a concerted push towards digital transformation and AI adoption across various industries, including automotive, industrial manufacturing, and scientific research. German automotive giants are heavily investing in autonomous driving technologies, which are incredibly compute-intensive and rely on advanced AI hardware. Similarly, European research institutions and universities are at the forefront of AI innovation, requiring powerful computing resources for their academic pursuits. The increasing focus on data privacy and sovereign AI initiatives within Europe might lead to a more localized demand for AI solutions, but the foundational hardware needs still heavily favor companies like Nvidia.

Other regions, including Canada, Japan, and emerging markets in Southeast Asia and Latin America, contribute to Nvidia’s global revenue, albeit at lower percentages. Canada’s growing AI research hubs and its adoption of AI in sectors like natural resources and finance are noteworthy. Japan’s advanced robotics and automotive sectors, coupled with a long-standing commitment to technological advancement, create a steady demand. As AI adoption becomes more widespread globally, these emerging markets represent future growth potential for Nvidia.

The fiscal year 2026 projections are not merely about geographical distribution but also reflect a fundamental shift in computing paradigms. Nvidia’s revenue is increasingly tied to the adoption of AI across the entire economic spectrum. The company’s Hopper architecture, and its successors, are designed to handle the immense computational loads required for training and deploying sophisticated AI models, making them essential for a new generation of digital services and products. This reliance on Nvidia’s specialized hardware positions the company as a critical enabler of the ongoing digital revolution, with its revenue streams intricately linked to the global pace of AI integration and innovation. The breakdown of revenue by customer headquarters, therefore, serves as a powerful indicator of where the most significant AI development and deployment activities are concentrated, and by extension, where Nvidia’s influence and financial success are most pronounced. The company’s ability to navigate geopolitical complexities, maintain its technological edge, and cater to the diverse needs of its global clientele will be paramount in shaping its financial trajectory in the coming fiscal years.