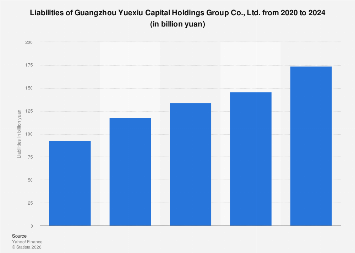

The financial health of major state-owned enterprises (SOEs) is a critical barometer for the broader economic stability and trajectory of their respective nations. Guangzhou Yuexiu Capital Holdings Group Co., Ltd. (GYCH), a prominent player in China’s financial services and urban development sectors, is no exception. As of 2024, a detailed examination of its liabilities offers crucial insights into its operational leverage, risk management strategies, and its capacity to navigate the dynamic global economic environment. Understanding the composition and evolution of GYCH’s debt is paramount for investors, creditors, policymakers, and market analysts seeking to assess its long-term solvency and growth potential.

While precise, granular data on GYCH’s liabilities for 2024 typically requires specialized access, the general trends and strategic imperatives surrounding Chinese SOE financing provide a robust framework for analysis. Historically, SOEs like GYCH have played a significant role in implementing national economic policies, often requiring substantial capital investment. This can translate into considerable balance sheet liabilities, encompassing various forms of debt, including bank loans, corporate bonds, and potentially inter-company borrowings, especially given its conglomerate structure. The sheer scale of its operations, which span financial services, infrastructure, and real estate, necessitates a continuous influx of capital, thereby shaping its liability profile.

The composition of GYCH’s liabilities in 2024 is likely to reflect a strategic balance between short-term operational needs and long-term developmental objectives. Short-term liabilities, such as accounts payable and short-term borrowings, are essential for maintaining day-to-day liquidity and covering immediate operational expenses. These are generally managed through robust treasury functions and access to revolving credit facilities. However, it is the structure and magnitude of long-term liabilities that provide a more telling narrative about the company’s investment strategy and its ability to service its obligations over extended periods. This category would typically include long-term bank loans, bonds issued to finance infrastructure projects, and potentially deferred tax liabilities.

The prevailing interest rate environment in China and globally significantly influences the cost of GYCH’s debt servicing. In periods of rising global interest rates, the cost of new borrowing increases, and the refinancing of existing debt can become more expensive. Conversely, a stable or declining interest rate environment can alleviate pressure on the company’s cash flow. Chinese monetary policy, managed by the People’s Bank of China, plays a pivotal role in shaping these conditions. The central bank’s directives on lending rates, reserve requirements, and liquidity injections directly impact the cost and availability of capital for entities like GYCH.

Furthermore, GYCH’s liability management is intrinsically linked to its asset base and profitability. A strong and growing asset portfolio, coupled with consistent profitability, provides the necessary foundation to absorb and service debt. Key financial metrics such as the debt-to-equity ratio, interest coverage ratio, and current ratio offer critical indicators of financial leverage and solvency. A rising debt-to-equity ratio, for instance, suggests an increased reliance on borrowed funds, which can amplify returns during periods of growth but also magnify losses during downturns. Conversely, a robust interest coverage ratio indicates the company’s ability to meet its interest obligations from its operating income.

The specific sectors in which GYCH operates also present unique liability considerations. Its involvement in financial services, for example, means that regulatory capital requirements and prudential norms significantly influence its borrowing capacity and the types of liabilities it can incur. In real estate and infrastructure, projects are often capital-intensive and have long gestation periods, necessitating long-term financing. The performance of these sectors, influenced by government policies, market demand, and macroeconomic conditions, directly impacts the revenue streams available to service the debt incurred for these ventures.

Globally, the trend of increasing corporate debt levels has been a point of discussion among economists. While leverage can fuel expansion, excessive debt poses systemic risks. For Chinese SOEs, there is often a dual mandate: to achieve commercial objectives while also serving national strategic goals. This can sometimes lead to financing decisions that might not purely be driven by market logic, potentially impacting their liability structure. However, recent years have seen a concerted effort by Chinese authorities to deleverage the corporate sector and enhance the financial discipline of SOEs, suggesting a move towards more sustainable financing practices.

The issuance of corporate bonds by GYCH, either domestically or potentially in international markets, represents another significant facet of its liability structure. The terms of these bonds, including coupon rates, maturity dates, and covenants, are crucial. Moody’s, Standard & Poor’s, and Fitch Ratings provide credit assessments that influence the pricing and accessibility of debt for large corporations. GYCH’s credit rating would be a key determinant of its ability to raise capital efficiently. The issuance of green bonds or social bonds, aligned with China’s sustainability objectives, could also be part of its financing strategy, offering diversified funding sources and potentially lower borrowing costs for projects with environmental or social benefits.

The economic impact of GYCH’s liability management extends beyond its own financial statements. As a major financial services provider, its stability underpins the broader financial system. Any distress in its debt servicing could have ripple effects on its creditors and the wider economy. Conversely, its ability to access capital efficiently and invest in key sectors can be a significant driver of economic growth and employment. Its role in urban development, for instance, directly contributes to infrastructure improvement and economic activity.

In conclusion, a comprehensive understanding of Guangzhou Yuexiu Capital Holdings Group’s liabilities in 2024 is not merely an academic exercise in financial accounting; it is a vital component of assessing its strategic positioning within China’s evolving economic landscape. The interplay of its operational scale, sector-specific demands, prevailing interest rate policies, and national economic objectives shapes its debt profile. While precise figures remain proprietary, the strategic management of its liabilities – balancing leverage for growth with the imperative of solvency and financial discipline – will be a defining factor in its continued success and its contribution to China’s economic development in the coming years. The ongoing trends towards deleveraging and enhanced corporate governance within China’s SOE sector suggest that GYCH, like its peers, is likely navigating a path that prioritizes both robust financial performance and long-term sustainability.