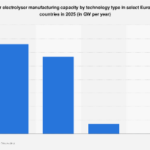

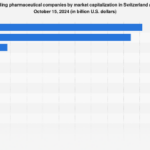

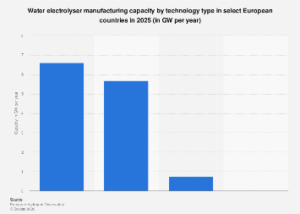

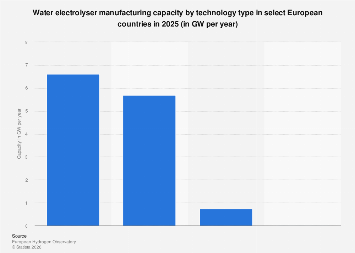

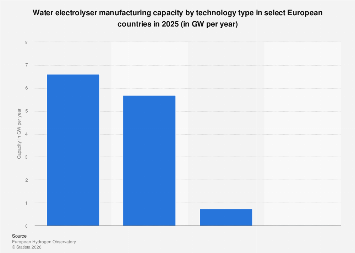

Europe is charting an ambitious course toward a hydrogen-powered future, with a significant expansion in water electrolyser manufacturing capacity expected by 2025. This burgeoning sector, crucial for producing green hydrogen through electrolysis powered by renewable energy, is projected to see Proton Exchange Membrane (PEM) technology emerge as the dominant force, accounting for over half of the continent’s total production capabilities.

The latest projections indicate that by 2025, Europe’s water electrolyser manufacturing capacity will reach a substantial figure, with PEM technology alone slated to contribute a significant portion. This advanced technology, known for its efficiency and suitability for variable renewable energy sources, is positioning itself as the cornerstone of Europe’s green hydrogen strategy. Alkaline electrolysis, a more established technology, will also play a vital role, representing a considerable share of the total capacity, underscoring a diversified approach to manufacturing. While specific figures for the exact gigawatt (GW) per year capacity are subject to proprietary market intelligence, the trend clearly points towards a robust build-out across the continent. This surge in manufacturing capability is not merely an isolated industrial development; it is a direct response to escalating climate targets and the urgent need to decarbonise hard-to-abate sectors such as heavy industry and long-haul transportation.

The strategic importance of developing a strong domestic electrolyser manufacturing base cannot be overstated. As nations across the European Union and the United Kingdom (EU27, Iceland, Liechtenstein, Norway, Switzerland, and the UK) commit to ambitious renewable energy targets and net-zero emissions goals, the demand for green hydrogen is set to skyrocket. This anticipated demand fuels the need for scaled-up production of electrolysers, the essential devices that split water molecules into hydrogen and oxygen using electricity. A robust manufacturing ecosystem within Europe will not only ensure a reliable supply chain for these critical components but also foster innovation, create high-skilled jobs, and reduce reliance on external suppliers, thereby enhancing energy security.

The dominance of PEM technology in Europe’s manufacturing landscape is a testament to its perceived advantages. PEM electrolysers offer faster response times, greater flexibility in operation, and a more compact design compared to traditional alkaline systems. These characteristics make them particularly well-suited for integration with intermittent renewable energy sources like solar and wind power, which are central to Europe’s decarbonisation strategy. The ability to quickly ramp up and down production in response to electricity availability is a key factor driving the preference for PEM in the context of a grid increasingly powered by renewables. Furthermore, ongoing research and development are continuously improving the cost-effectiveness and durability of PEM electrolysers, further solidifying their competitive edge.

However, alkaline electrolysis remains a significant player, and its continued presence in the market highlights its own inherent strengths. Alkaline electrolysers are generally more mature, have a longer track record of reliability, and often present a lower upfront capital cost, especially for large-scale, baseload operations where energy price volatility is less of a concern. The synergy between PEM and alkaline technologies allows for a more comprehensive approach to hydrogen production, catering to diverse applications and operational requirements across different industrial settings and geographical regions within Europe. This dual-technology approach provides flexibility and resilience to the overall European hydrogen infrastructure development.

The geographical distribution of this manufacturing capacity across select European countries is a critical aspect of the continent’s hydrogen strategy. While specific country-level data remains largely proprietary, it is understood that key industrial hubs and nations with strong renewable energy potential are likely to emerge as leaders in electrolyser production. Countries with established chemical and engineering industries, coupled with supportive government policies and incentives, are poised to attract significant investment in manufacturing facilities. This could include nations like Germany, France, Spain, and the Netherlands, among others, which are actively pursuing ambitious hydrogen roadmaps. The development of these manufacturing clusters will not only serve domestic demand but also position Europe as a significant exporter of electrolyser technology on the global stage.

The economic implications of this expansion are far-reaching. The growth of the water electrolyser manufacturing sector is expected to create thousands of direct and indirect jobs, spanning research and development, engineering, manufacturing, installation, and maintenance. This burgeoning industry has the potential to revitalise industrial regions, foster technological innovation, and contribute significantly to Europe’s GDP. Moreover, the widespread adoption of green hydrogen produced by these electrolysers will enable deep decarbonisation across critical sectors, helping Europe meet its climate targets and enhance its competitiveness in a global economy increasingly focused on sustainability. The ripple effect will extend to downstream industries that can leverage green hydrogen as a clean fuel and feedstock, such as steel production, ammonia synthesis, and synthetic fuel manufacturing.

Global comparisons further underscore the significance of Europe’s efforts. While China currently leads in overall electrolyser manufacturing capacity, Europe is making substantial strides in establishing a high-quality, technologically advanced production base, particularly with a focus on PEM technology. The European Union’s Hydrogen Strategy and the REPowerEU plan explicitly target the scaling up of domestic electrolyser manufacturing to reduce import dependency and secure a leading role in the global hydrogen economy. This strategic foresight positions Europe not just as a consumer of hydrogen technology but as a key innovator and producer, capable of influencing global standards and driving down costs through economies of scale and technological advancement.

The investment landscape for electrolyser manufacturing in Europe is also experiencing a significant uplift. Numerous announcements of new factories, expansions of existing facilities, and strategic partnerships between technology providers, industrial conglomerates, and energy companies signal strong investor confidence. Government grants, subsidies, and tax incentives are playing a crucial role in de-risking investments and accelerating the pace of capacity build-out. However, challenges remain, including the need for further cost reductions in electrolyser technology, the development of robust hydrogen infrastructure (including pipelines and storage), and the establishment of stable regulatory frameworks that provide long-term certainty for investors and off-takers.

In conclusion, the projected growth in Europe’s water electrolyser manufacturing capacity by 2025, with PEM technology at the forefront, represents a critical inflection point in the continent’s journey towards a sustainable energy future. This expansion is underpinned by a confluence of strong political will, technological innovation, and increasing market demand. As Europe bolsters its domestic production capabilities, it not only paves the way for widespread green hydrogen adoption but also solidifies its position as a global leader in the clean energy transition, fostering economic growth and enhancing energy independence. The coming years will be pivotal in transforming these manufacturing ambitions into tangible realities, shaping the future of energy and industry across the continent and beyond.