The United Kingdom’s sovereign bond market is currently grappling with a renewed wave of volatility, as government debt prices tumble and yields climb to levels that underscore a growing anxiety among global investors. This deepening slump in the gilt market reflects a significant recalibration of expectations regarding the Bank of England’s (BoE) monetary policy trajectory. While many had entered the year anticipating a swift pivot toward interest rate reductions, the reality of "sticky" inflation and a resilient labor market has forced a painful repricing of risk. Traders are now increasingly betting that the central bank will be forced to maintain a restrictive stance for longer than previously forecasted, or perhaps even consider further tightening if price pressures fail to abate.

The sell-off in gilts is not an isolated event but rather the culmination of several converging economic factors. Primarily, the most recent tranches of data concerning Consumer Price Index (CPI) inflation and wage growth have surprised to the upside. In the complex machinery of the British economy, services inflation remains the most stubborn component, refusing to settle back toward the Bank of England’s 2% target with the alacrity that policymakers had hoped for. This persistence in the services sector, which accounts for roughly 80% of the UK’s economic output, suggests that domestic price pressures are becoming entrenched, potentially requiring a more prolonged period of high interest rates to cool.

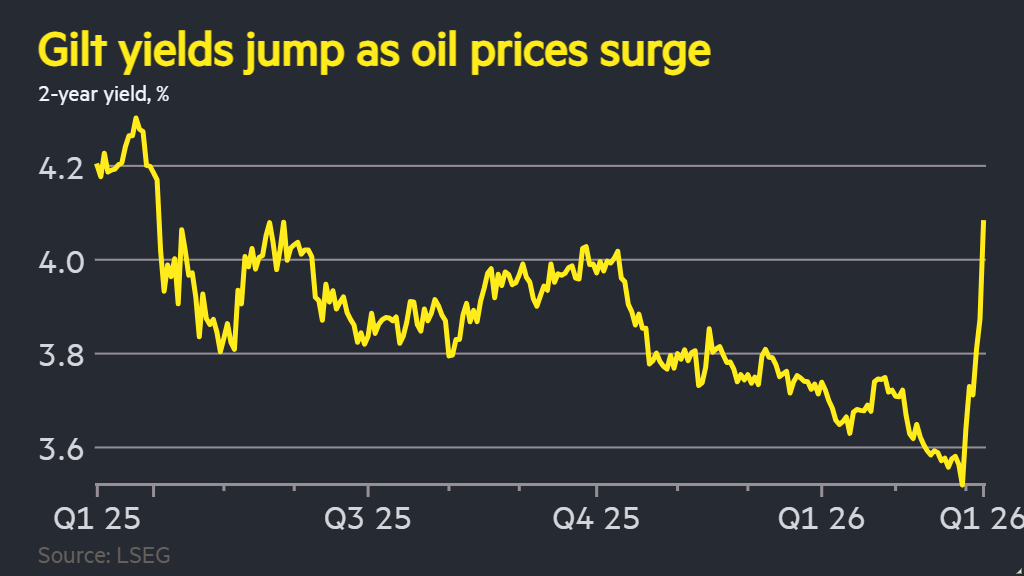

In the bond market, the reaction has been swift and unforgiving. The yield on the benchmark 10-year gilt, a critical barometer for the cost of borrowing across the wider economy, has surged as investors demand higher returns to compensate for the eroding effects of inflation and the prospect of a more hawkish central bank. Because bond prices move inversely to yields, this rise represents a significant loss in value for existing holders of government debt, ranging from pension funds to international sovereign wealth funds. The two-year gilt yield, which is particularly sensitive to changes in short-term interest rate expectations, has also seen a marked increase, reflecting the market’s conviction that the "higher for longer" narrative is now the dominant reality.

Central to this market turmoil is the shifting sentiment within the Bank of England’s Monetary Policy Committee (MPC). Recent communications from Governor Andrew Bailey and other senior officials have been characterized by a tone of "cautious vigilance." While the BoE has acknowledged that the era of aggressive rate hikes may be in the rearview mirror, it has been equally firm in stating that it is too early to declare victory over inflation. The divergence in voting patterns among MPC members—with some advocating for immediate cuts and others still concerned about the need for further hikes—has created a sense of uncertainty that markets rarely tolerate well. This ambiguity has fueled the current slump, as traders hedge against the possibility that the UK may be an outlier among G7 nations in its struggle to contain price growth.

Comparing the UK’s situation to its international peers reveals a challenging landscape. While the US Federal Reserve and the European Central Bank (ECB) are facing similar dilemmas, the UK’s "inflation premium" appears more pronounced. Structural issues, including a post-Brexit labor shortage and a heavy reliance on imported energy and food, have made the British economy more susceptible to supply-side shocks. Consequently, while US Treasuries and German Bunds have also seen yields rise, the volatility in the gilt market has often outpaced its counterparts, suggesting that investors perceive a higher degree of risk in the UK’s fiscal and monetary outlook.

The implications of rising gilt yields extend far beyond the trading floors of the City of London. The most immediate impact is felt in the mortgage market. Most UK lenders price their fixed-rate mortgage products based on "swap rates," which are directly influenced by gilt yields. As yields climb, the cost for banks to hedge their lending increases, a cost that is invariably passed on to consumers. For millions of British households facing the "mortgage cliff"—the expiration of low-rate deals secured years ago—the current market slump represents a direct threat to disposable income and consumer spending. This creates a precarious feedback loop: higher rates are needed to fight inflation, but those same rates risk tipping a fragile economy into a deeper recession.

Furthermore, the fiscal position of the UK government is being squeezed. As the yield on government debt rises, the cost of servicing that debt increases. For the Treasury, this means a larger portion of tax revenue must be diverted toward interest payments rather than public services or infrastructure investment. With the national debt hovering around 100% of GDP, the sensitivity of the public finances to even small movements in interest rates is acute. This fiscal drag limits the government’s room for maneuver, particularly in an election year when pressure to announce tax cuts or spending increases is at its peak.

Institutional investors are also reassessing their portfolios in light of the gilt market’s performance. For years, government bonds were viewed as the ultimate "safe haven" asset, providing a reliable hedge against equity market volatility. However, the correlation between stocks and bonds has shifted in the current inflationary environment, with both asset classes often falling in tandem. This has led to a broader "de-risking" strategy among fund managers, who are now looking toward alternative assets or higher-yielding corporate credit, further draining liquidity from the gilt market and exacerbating the downward pressure on prices.

Economists are closely monitoring the "yield curve," which provides a snapshot of investor expectations for the economy over different time horizons. An inverted yield curve—where short-term yields are higher than long-term yields—has historically been a harbinger of recession. While the UK curve has flirted with inversion, the recent parallel shift upward suggests a market that is less focused on a looming crash and more concerned with a period of "stagflation": stagnant growth coupled with high inflation. This is perhaps the most difficult scenario for a central bank to manage, as the traditional tools used to stimulate growth (cutting rates) would only serve to further ignite inflationary pressures.

The role of Quantitative Tightening (QT) cannot be overlooked in this analysis. The Bank of England is currently in the process of unwinding its massive balance sheet, accumulated through years of bond-buying programs. By selling gilts back into the market or allowing them to mature without reinvesting the proceeds, the BoE is effectively increasing the supply of bonds at a time when demand is already wavering. This technical factor adds another layer of upward pressure on yields, complicating the Treasury’s efforts to manage the national debt and ensuring that the market remains sensitive to even minor shifts in liquidity.

Looking ahead, the path for the gilt market remains fraught with uncertainty. The upcoming releases of labor market data and monthly GDP figures will be critical in determining whether the BoE can find a window to begin easing policy. If wage growth remains near 6% and the unemployment rate stays historically low, the MPC will find it nearly impossible to justify a rate cut without risking a secondary spike in inflation. Conversely, if the economy shows signs of significant cracking under the weight of current rates, the central bank may be forced to act, even if inflation remains above the target.

In summary, the deepening slump in the gilt market is a clear signal that the transition from a decade of ultra-low interest rates to a new economic equilibrium is proving to be both volatile and painful. Investors are no longer giving the Bank of England the benefit of the doubt, demanding instead concrete evidence that inflation is truly under control before returning to the bond market in earnest. As the UK navigates this period of economic recalibration, the gilt market will remain the primary stage upon which the tension between monetary necessity and fiscal reality is played out, with profound consequences for the British economy and the global financial landscape.