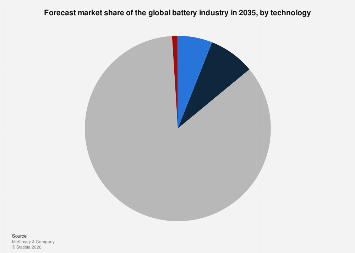

The global energy storage sector is poised for a dramatic transformation by 2035, with projections indicating significant shifts in the market share of various battery technologies. While lithium-ion batteries currently dominate the market, driven by their widespread adoption in electric vehicles (EVs) and consumer electronics, a diverse array of emerging and advanced battery chemistries are set to challenge this status quo. Understanding these technological trajectories is crucial for investors, manufacturers, and policymakers navigating the rapidly evolving energy landscape.

The dominance of lithium-ion batteries, particularly lithium-iron-phosphate (LFP) and nickel-manganese-cobalt (NMC) variants, is expected to continue for the foreseeable future. LFP, known for its enhanced safety, longer lifespan, and lower cost due to the absence of cobalt, has gained considerable traction, especially in the automotive sector and for grid-scale energy storage solutions. Companies are investing heavily in expanding LFP production capacity to meet surging demand, making it a cost-effective and sustainable choice for many applications. NMC chemistries, while offering higher energy density crucial for longer-range EVs, face ongoing scrutiny regarding the ethical sourcing of cobalt and nickel, prompting research into alternative cathode materials.

However, the next decade and a half will witness the ascendance of several promising technologies. Solid-state batteries represent a significant leap forward, promising enhanced safety by replacing flammable liquid electrolytes with solid materials. This innovation could unlock higher energy densities, faster charging times, and improved thermal stability, making them particularly attractive for the premium EV market and next-generation portable electronics. Several major automotive manufacturers and battery developers have announced ambitious timelines for commercializing solid-state batteries, with some initial applications expected within the next five years. The challenge, however, lies in scaling up production affordably and achieving consistent performance across large manufacturing volumes. Market analysts predict that solid-state batteries could capture a substantial, albeit initially niche, market share by 2035, particularly in high-performance applications where safety and energy density are paramount.

Another area of intense development is sodium-ion (Na-ion) battery technology. Leveraging the abundant and low-cost nature of sodium, these batteries offer a compelling alternative, especially for stationary energy storage and potentially for entry-level EVs. While historically plagued by lower energy density compared to lithium-ion, recent advancements in cathode and electrolyte materials are rapidly closing this gap. The cost-effectiveness and sustainability of Na-ion batteries, which avoid reliance on critical minerals like lithium and cobalt, position them as a strong contender for grid-scale storage projects and for applications where extreme energy density is not the primary requirement. Projections suggest that Na-ion batteries could carve out a significant portion of the stationary storage market by 2035, potentially competing with LFP in certain segments.

Beyond these, research into next-generation chemistries continues unabated. Flow batteries, for instance, are gaining attention for their scalability and long-duration storage capabilities, making them ideal for grid-scale applications requiring the storage of large amounts of energy for extended periods. Their modular design allows for independent scaling of power and energy capacity, offering flexibility for utility-scale projects. While currently more expensive than conventional battery technologies, ongoing innovation is driving down costs. Metal-air batteries, such as lithium-air and zinc-air, hold the theoretical promise of extremely high energy densities, potentially exceeding those of lithium-ion batteries by a significant margin. However, these technologies face substantial technical hurdles related to cycle life, efficiency, and cost-effective manufacturing, making their widespread commercialization by 2035 less certain, though early niche applications might emerge.

The global market for batteries is projected to experience exponential growth. Projections from various market research firms indicate that the total battery market could reach well over $500 billion annually by 2030, with further expansion beyond that point. This growth is primarily fueled by the burgeoning electric vehicle market, which is increasingly mandated and incentivized by governments worldwide to meet climate targets. The International Energy Agency (IEA) has consistently highlighted the critical role of battery technology in achieving decarbonization goals, emphasizing the need for both increased production capacity and diversification of battery chemistries to ensure supply chain resilience and affordability.

The geographic distribution of battery production is also undergoing a significant shift. While China has long been the dominant force in battery manufacturing, North America and Europe are making concerted efforts to establish robust domestic battery supply chains. This push is driven by a desire to reduce reliance on single-source suppliers, enhance energy security, and capitalize on the economic opportunities presented by the clean energy transition. Investments in gigafactories for lithium-ion and emerging battery technologies are being announced at an unprecedented pace across these regions. This diversification of manufacturing hubs could lead to regional variations in the adoption of specific battery technologies based on local resource availability, policy incentives, and industrial strengths.

The economic implications of these technological shifts are profound. The race to develop and commercialize advanced battery technologies is spurring innovation and creating new markets for raw materials, manufacturing equipment, and skilled labor. Companies that can successfully navigate the complex technological and manufacturing challenges of these next-generation batteries stand to gain a significant competitive advantage. Furthermore, the widespread deployment of diverse and cost-effective energy storage solutions is essential for integrating intermittent renewable energy sources like solar and wind into the grid, thereby accelerating the transition away from fossil fuels. The ability to store and dispatch clean energy reliably is a cornerstone of a sustainable and secure energy future.

Challenges, however, remain. The sourcing of raw materials, including lithium, cobalt, nickel, and rare earth elements, continues to be a point of concern. Geopolitical considerations, environmental impacts of extraction, and price volatility are driving efforts to improve recycling processes and develop batteries that utilize more abundant and ethically sourced materials. The circular economy for batteries, through robust recycling infrastructure and second-life applications, will be crucial for ensuring the long-term sustainability of the industry. Moreover, the development of standardized testing protocols and regulatory frameworks for new battery technologies will be vital for fostering market confidence and ensuring safety.

In conclusion, the battery technology landscape by 2035 will likely be characterized by a more diversified portfolio than today. While lithium-ion batteries will remain a significant player, particularly LFP, solid-state and sodium-ion batteries are poised to capture substantial market share in key applications. The continuous innovation in materials science and manufacturing processes will drive down costs, improve performance, and unlock new possibilities for energy storage, playing a pivotal role in the global transition to a low-carbon economy. The strategic investments, policy support, and ongoing research and development efforts across the globe will shape which technologies ultimately lead the charge in this critical sector.