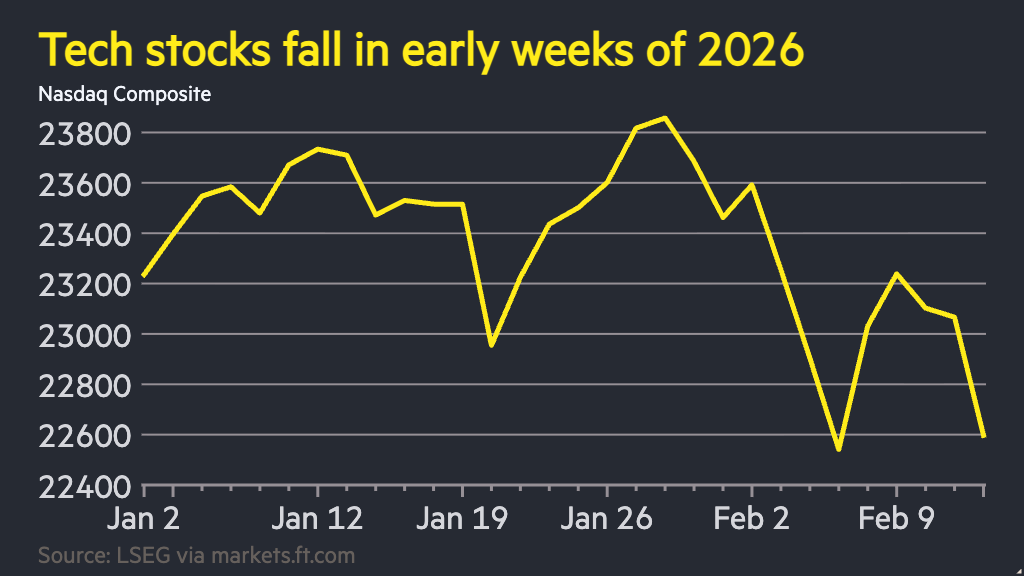

The euphoric momentum that propelled American equity markets to record highs throughout the first half of the year has encountered a formidable wall of resistance, as a renewed sell-off in the technology sector sent shockwaves through Wall Street. On a day characterized by heightened volatility and a palpable shift in investor sentiment, the Nasdaq Composite plummeted, dragging the broader S&P 500 into the red and raising urgent questions about the sustainability of the artificial intelligence-driven rally that has defined the 2024 fiscal landscape. This sharp correction reflects a growing consensus among institutional investors that the "AI premium"—the elevated valuation multiples assigned to tech giants—may have outpaced the immediate earnings potential of these burgeoning technologies.

The downward pressure was felt most acutely among the so-called "Magnificent Seven," the cohort of mega-cap technology stocks that includes Nvidia, Apple, Microsoft, Alphabet, Amazon, Meta, and Tesla. For months, these firms acted as the primary engines of market growth, accounting for a disproportionate share of the S&P 500’s total returns. However, the concentration of wealth in these few entities has created a precarious market structure. When sentiment sours in the semiconductor or software-as-a-service sectors, the impact is no longer localized; it reverberates across the entire financial ecosystem. Analysts note that the current retreat is less a sign of fundamental failure and more a "valuation reset," as the market grapples with the high cost of capital and the realization that the transition to an AI-integrated economy will be a marathon rather than a sprint.

Economic indicators released earlier in the week have added fuel to the fire. While inflation appears to be cooling—bringing the Federal Reserve’s 2% target into view—the softening of the labor market has introduced a new set of anxieties. The latest payroll data suggested a more pronounced slowdown in hiring than previously anticipated, triggering the "Sahm Rule," a historically reliable recession indicator that tracks the rise in the unemployment rate. Consequently, the narrative in the trading pits has shifted from "inflation concerns" to "growth concerns." Investors who were once eager to pay any price for a piece of the AI future are now rotating their portfolios into defensive sectors, such as utilities, healthcare, and consumer staples, seeking refuge from the cyclical volatility of high-tech growth.

The semiconductor industry, often viewed as the bellwether for the modern economy, bore the brunt of the day’s losses. Nvidia, which had briefly claimed the title of the world’s most valuable company earlier this year, saw its market capitalization contract significantly as traders locked in profits. The sell-off was exacerbated by reports of tightening export controls on high-end chips and a growing skepticism regarding the massive capital expenditure (CAPEX) budgets of major cloud providers. While companies like Microsoft and Google continue to pour billions into data centers and specialized hardware, shareholders are beginning to demand clearer timelines for when these investments will translate into bottom-line profitability. The "Show Me the Money" phase of the AI cycle has officially begun, and any company failing to provide a concrete roadmap for monetization is being punished by the markets.

Beyond the borders of the United States, the tremors from the tech sell-off were felt in international hubs. In Tokyo, the Nikkei 225 experienced a sympathetic decline, particularly among chip-equipment manufacturers that are deeply integrated into the American supply chain. Similarly, the European STOXX 600 technology index saw its sharpest one-day drop in months, as global fund managers reduced their exposure to growth-oriented equities. This synchronized retreat underscores the interconnectedness of global capital markets; a sneeze in Silicon Valley often results in a cold for the entire global tech sector. Furthermore, the strengthening of the Japanese Yen has led to a partial unwinding of the "carry trade," a financial maneuver where investors borrow in low-interest currencies to invest in high-yielding assets like US tech stocks. As this trade reverses, it creates a feedback loop of selling pressure that is difficult to arrest.

The fixed-income market has provided little solace for those looking for stability. The yield on the 10-year Treasury note, a critical benchmark for corporate borrowing costs, has fluctuated wildly as investors attempt to front-run the Federal Reserve’s next move. While a series of interest rate cuts is widely expected before the end of the year, the motivation behind such cuts is now under scrutiny. If the Fed cuts rates because inflation is conquered, the markets may react positively. However, if the Fed is perceived to be cutting rates in a "panic" to prevent a hard landing for the economy, the move could be interpreted as a confirmation of underlying systemic weakness. This ambiguity has left the CBOE Volatility Index (VIX), commonly known as the market’s "fear gauge," at its highest level in several months, indicating that the period of low-volatility "easy gains" is likely over.

From a technical perspective, the S&P 500 and the Nasdaq are testing key support levels. Chartists and quantitative analysts are closely watching the 50-day and 200-day moving averages; a sustained break below these levels could trigger algorithmic selling programs, further accelerating the decline. Margin calls for retail investors who entered the market at the peak of the AI hype are also a concern, as forced liquidations can create "air pockets" in the market where prices drop precipitously due to a lack of buyers. The current environment is a stark reminder of the "mean reversion" principle in finance—the idea that assets eventually return to their long-term average valuations after a period of extreme overperformance.

Despite the prevailing gloom, some veteran market participants view this correction as a necessary and healthy development. The parabolic rise of tech stocks had created a "crowded trade," where almost every institutional portfolio was overweight in the same handful of names. A washout of this nature flushes out speculative excess and allows for a more rational allocation of capital. It also provides an opportunity for "sector rotation," where the broader market—including small-cap stocks and traditional industrial firms—can finally participate in the rally. The Russell 2000 index, which tracks smaller companies, has shown flashes of resilience, suggesting that the "Great Rotation" from mega-cap tech to the "rest of the market" may finally be underway.

The economic impact of a sustained tech downturn extends beyond brokerage accounts. Silicon Valley is a major driver of tax revenue, venture capital investment, and high-wage employment. A significant decline in market valuations can lead to a cooling of the "wealth effect," where consumers feel less wealthy and therefore reduce their discretionary spending. This, in turn, can dampen GDP growth. For the Federal Reserve, the challenge is now one of precision: they must balance the need to maintain restrictive enough rates to ensure inflation does not rebound, while providing enough liquidity to prevent a market correction from metastasizing into a full-blown financial crisis.

Looking ahead, the upcoming earnings season will be the ultimate arbiter of market direction. Investors will be scrutinizing quarterly reports not just for revenue beats, but for guidance on how companies intend to navigate a higher-for-longer interest rate environment and a potential slowdown in consumer demand. The narrative that "AI will solve everything" is no longer sufficient to support a 30x price-to-earnings ratio. Companies will need to demonstrate operational efficiency, pricing power, and a resilient supply chain to regain the trust of a now-skeptical market.

In conclusion, the sharp fall in US stocks marks a transition point for the post-pandemic economy. The era of unbridled optimism regarding the immediate transformative power of AI is giving way to a more sober, data-driven assessment of economic reality. While the long-term prospects for technology remain bright, the path forward is likely to be characterized by greater volatility, more rigorous valuation standards, and a renewed focus on the health of the broader macroeconomy. As the dust settles on this latest sell-off, the primary objective for investors will be distinguishing between a temporary dip in a long-term bull market and the beginning of a more profound structural shift in the global financial landscape.