The traditional paradigms for managing supply chain vulnerabilities, often honed against the predictable ebbs and flows of natural disasters, isolated supplier failures, or cyclical market volatility, are proving woefully inadequate in the current era. A new, more insidious class of disruption has emerged, driven by persistent and often politically motivated geopolitical events such as escalating trade disputes, punitive sanctions regimes, and outright armed conflicts. Global enterprises, accustomed to optimizing for efficiency and cost-effectiveness in a largely interconnected world, are now grappling with an unprecedented level of complexity and uncertainty, struggling to forge effective responses to maneuvers by national leaders that ripple through their intricate networks.

At the core of this evolving challenge lies a profound dual burden: the sheer complexity of modern supply chains interwoven across continents, and the inherent unpredictability of geopolitical forces. Long-established international trade policies, once considered stable bedrock, have become fluid and subject to abrupt shifts, exemplified by the rapid imposition and removal of tariffs, export controls, and import restrictions. Acts of war or state-sponsored terrorism can fundamentally alter an executive’s assumptions about security and operational risk overnight, as seen with recent conflicts that have rerouted shipping lanes, disrupted energy supplies, and severed critical manufacturing hubs. The vast scale and intricate interdependencies within contemporary supply chains make it exceedingly difficult for companies to accurately forecast the cascade effect of such events across their entire operational footprint, from raw material sourcing to final product delivery.

In this environment, where the conventional playbook is increasingly obsolete, a more systematic and strategic approach to understanding, monitoring, and managing geopolitical risks is not merely advisable but critical for sustained viability. Leading organizations are recognizing that while there is no universal panacea or guaranteed outcome, a common thread among those demonstrating superior resilience is a relentless pursuit of end-to-end visibility across their entire supply chain ecosystem. These firms prioritize understanding the contributions and inherent risks associated with every supplier, sub-supplier, and customer, often extending far beyond their immediate tier-one partners. While achieving a complete, granular picture remains challenging due to data fragmentation and proprietary information, these companies are making concerted efforts to remain exceptionally well-informed, proactively cultivating alternative options for flexibility, and dynamically adapting their procurement and logistics networks as circumstances demand.

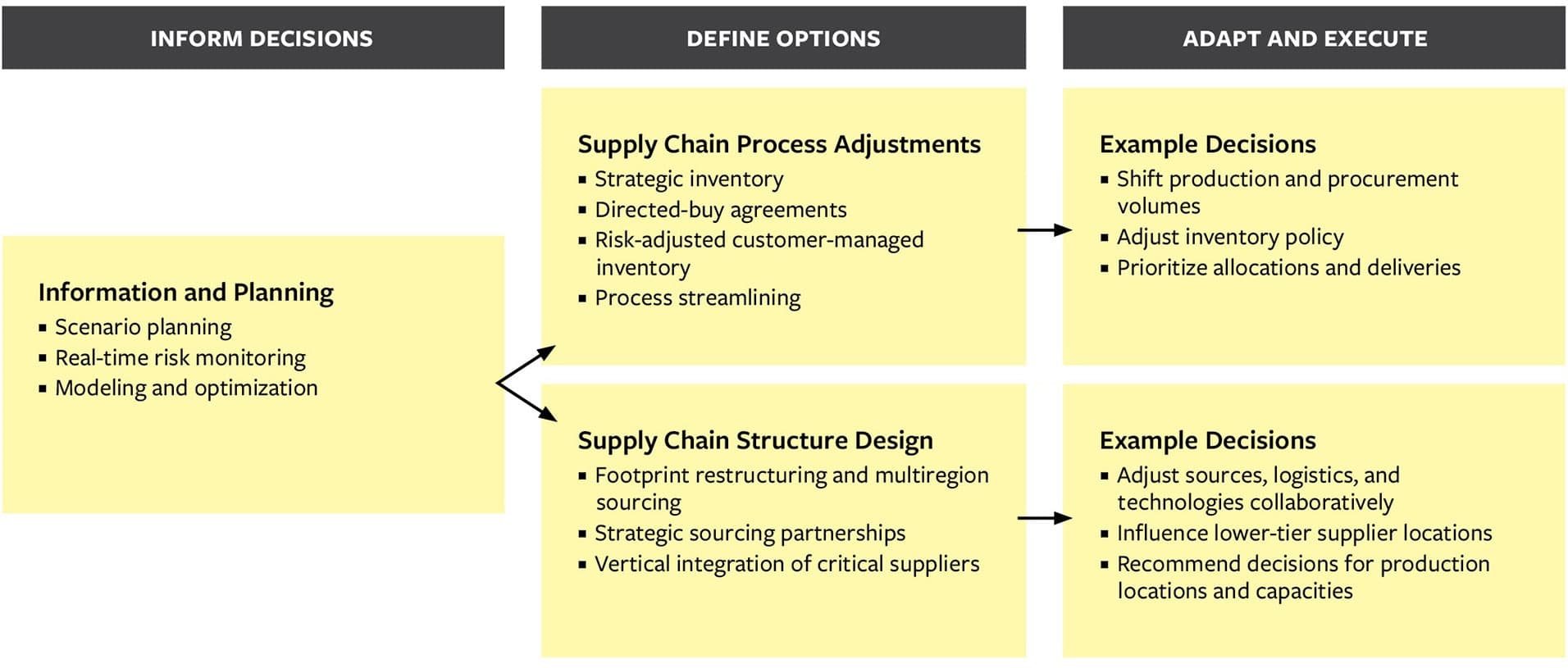

A comprehensive framework, developed from insights gleaned through the study of numerous multinational corporations, offers a structured approach for managers to navigate these constantly shifting conditions. This framework outlines three interdependent pillars designed to help businesses sense geopolitical signals, strategically anticipate and mitigate supply chain risks before they escalate, and adapt swiftly and effectively to unfolding events on the ground.

The first pillar, Understanding Geopolitical Signals, emphasizes proactive intelligence gathering and scenario planning. This moves beyond merely reacting to headlines, requiring a deep dive into potential future states shaped by geopolitical dynamics. Companies are advised to establish dedicated teams, often cross-functional and drawing expertise from international relations, economics, and logistics, to conduct rigorous scenario planning exercises. These exercises simulate various geopolitical eventualities—such as the full-scale decoupling of major economies, the emergence of new protectionist trade blocs, or the prolonged disruption of critical maritime routes—and assess their potential impact on specific supply chain nodes. For instance, simulating a major conflict in Southeast Asia could reveal critical dependencies on semiconductor manufacturing in the region, prompting proactive measures. Concurrently, robust risk monitoring systems are essential. These leverage advanced analytics and artificial intelligence to continuously track a broad spectrum of indicators, including political stability indices, economic sanctions databases, trade policy changes, commodity price fluctuations, and even social unrest metrics, providing early warnings of impending disruptions. Investment in geopolitical intelligence platforms and partnerships with specialized consultancies can significantly enhance a firm’s ability to interpret these complex signals and identify emerging vulnerabilities, transforming raw data into actionable insights.

The second pillar focuses on Anticipating Risks by Creating Flexible Options. Once potential risks are identified, the strategic imperative shifts to building inherent resilience and optionality into the supply chain design. This involves moving away from the "just-in-time" philosophy, which prioritizes lean inventory and single-source efficiency, towards a more "just-in-case" approach that values redundancy and strategic diversification. Key strategies include geographic diversification of sourcing and manufacturing, often manifesting as "China+1" strategies or the exploration of nearshoring and reshoring initiatives to reduce reliance on single regions or political jurisdictions. For example, automotive manufacturers might dual-source critical electronic components from both East Asia and Eastern Europe to hedge against regional instability. Building redundancy also extends to maintaining strategic buffer stocks of critical raw materials or finished goods, albeit at a higher carrying cost, and qualifying multiple suppliers for essential components, even if alternative suppliers are initially more expensive. Furthermore, designing products with modularity and interchangeable components can provide significant agility, allowing production lines to pivot quickly to alternative parts if a primary source becomes unavailable. Establishing strategic partnerships with logistics providers, government agencies, and even competitors for contingency planning also falls under this pillar, fostering a collective resilience network. The economic rationale here is a trade-off: higher upfront investment in resilience measures against the potentially far greater costs of unmitigated disruption, which can include lost sales, reputational damage, and erosion of market share.

Finally, the third pillar, Adapting Quickly to Disruptions, addresses the necessary agility and responsiveness when geopolitical events inevitably materialize. This requires pre-established crisis management protocols, clear lines of communication, and delegated decision-making authority to enable rapid deployment of contingency plans. When a disruption hits, such as a sudden closure of a key port or the imposition of new tariffs, companies with well-defined response frameworks can activate alternative shipping routes, re-allocate production capacity across different facilities, or draw upon diversified inventory pools. The ability to dynamically re-route logistics, shift orders between suppliers, or even temporarily adjust product specifications to accommodate available components becomes paramount. Beyond immediate tactical responses, this pillar also emphasizes continuous learning and refinement. Post-mortem analyses of disruptions, whether successfully mitigated or not, are crucial for embedding lessons learned into future scenario planning, updating risk models, and refining supply chain strategies. This iterative process of sensing, anticipating, and adapting ensures that the organization’s resilience capabilities evolve in lockstep with the ever-changing geopolitical landscape.

The economic implications of neglecting geopolitical supply chain risks are profound and multifaceted. A study by the World Economic Forum estimated that supply chain disruptions cost companies an average of 42% of a year’s EBITDA every decade, with geopolitical events contributing significantly to this figure. The increased cost of logistics, driven by rerouting, longer lead times, and higher insurance premiums, directly impacts profitability and can fuel inflationary pressures across economies. Industries such as semiconductors, rare earth minerals, pharmaceuticals, and critical battery components are particularly susceptible, given their concentrated production footprints and strategic importance. Governments, too, are increasingly playing a role, with industrial policies and subsidies aimed at promoting reshoring and diversifying critical supply chains, reflecting a global trend towards economic nationalism and strategic autonomy. This shift is reshaping global trade patterns, potentially leading to regionalized supply blocs and a more fragmented, albeit potentially more secure, global economy.

Ultimately, mastering geopolitical supply chain risk is no longer a peripheral concern for corporate strategy; it is a central imperative for competitive advantage and long-term survival in a world characterized by continuous flux. Businesses that embed a sophisticated, multi-faceted approach to sensing, anticipating, and adapting to geopolitical realities will be better positioned not only to weather storms but also to identify new opportunities in a fractured global landscape. This demands a fundamental shift in mindset, from viewing supply chains purely as cost centers to recognizing them as strategic assets whose resilience directly underpins enterprise value and market leadership.