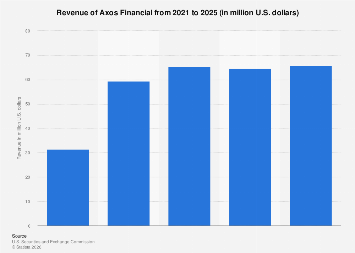

Axos Financial is poised for continued revenue expansion, with projections indicating a robust growth trajectory through the fiscal year 2025. This outlook is underpinned by the company’s strategic focus on digital banking innovation, its diversified revenue streams, and its ability to capitalize on evolving consumer preferences for streamlined, online financial services. While specific year-end revenue figures for fiscal year 2025 are subject to market fluctuations and the company’s ongoing performance, financial analysts and industry observers anticipate a sustained upward trend, reflecting Axos’s increasing market share and its adeptness at navigating the competitive landscape of the financial technology sector.

The company’s core business model, centered around its digital-first approach, has proven highly effective. Axos Bank, its primary operating subsidiary, offers a comprehensive suite of banking products, including high-yield savings accounts, checking accounts with competitive interest rates, and a growing portfolio of lending services, such as mortgages and small business loans. This digital infrastructure allows Axos to operate with a lower overhead compared to traditional brick-and-mortar institutions, enabling it to offer more attractive rates to customers and maintain healthy profit margins. The increasing adoption of online banking globally, accelerated by technological advancements and changing consumer habits, provides a fertile ground for Axos’s continued revenue generation. In the United States alone, the percentage of consumers who primarily use online banking has steadily climbed, with projections suggesting this trend will persist. This shift in consumer behavior directly translates into greater customer acquisition and retention for digital-native banks like Axos.

Furthermore, Axos Financial has strategically diversified its revenue generation beyond traditional deposit-taking and lending. The company has made significant inroads into the mortgage lending sector, both for consumers and through its wholesale and correspondent lending channels. This diversification not only broadens its customer base but also provides a hedge against potential downturns in specific market segments. The mortgage market, while cyclical, represents a substantial opportunity, and Axos’s ability to originate and service these loans efficiently contributes significantly to its overall revenue. Data from the Mortgage Bankers Association consistently shows the substantial volume of mortgage originations, and Axos’s growing presence in this space underscores its revenue potential.

Beyond mortgages, Axos also generates revenue through its investment and trading platforms, offering clients access to various financial instruments. While this segment may be more volatile than core banking operations, it adds another layer of revenue diversification and appeals to a different customer demographic. The growth in retail investing, particularly among younger generations, presents an ongoing opportunity for Axos to capture market share in this area. As commission-free trading and accessible investment tools become more prevalent, platforms like Axos’s are well-positioned to benefit.

The company’s financial performance is also influenced by broader economic factors, including interest rate environments, regulatory changes, and the overall health of the U.S. economy. Axos, like all financial institutions, is sensitive to shifts in monetary policy. When interest rates rise, banks typically benefit from an increased net interest margin – the difference between the interest income generated and the interest paid out. Conversely, periods of declining interest rates can compress these margins. However, Axos’s diversified revenue streams, particularly its fee-based income from mortgage origination and other services, can help mitigate the impact of interest rate fluctuations on its overall profitability.

In the global context, Axos operates within a financial services industry that is undergoing rapid digital transformation. While Axos is primarily focused on the U.S. market, the trends it embodies – a move towards digital, customer-centric banking – are universal. Competitors in other developed markets, such as challenger banks in Europe and Asia, are also leveraging technology to disrupt traditional banking models. This global shift validates Axos’s strategic direction and suggests a long-term favorable environment for its business model. The increasing penetration of digital payment systems and the growing demand for personalized financial advice delivered through digital channels further underscore the global relevance of Axos’s offerings.

Analysts often look at key performance indicators (KPIs) such as net interest income, non-interest income, efficiency ratios, and asset growth to assess a bank’s financial health and future prospects. Axos Financial has demonstrated consistent improvement in many of these metrics. Its ability to control operating expenses, largely due to its digital infrastructure, contributes to a strong efficiency ratio, meaning it generates more revenue per dollar of expense. This operational efficiency is a critical driver of profitability and supports sustained revenue growth.

Looking ahead to fiscal year 2025, several factors are likely to shape Axos’s revenue. Continued technological investment will be crucial for maintaining its competitive edge. This includes enhancing its mobile banking app, further developing its artificial intelligence capabilities for customer service and risk management, and ensuring robust cybersecurity measures to protect customer data and maintain trust. The company’s commitment to innovation is a recurring theme in its investor communications and is likely to be a key differentiator.

Moreover, strategic partnerships and potential acquisitions could also play a role in expanding Axos’s reach and revenue base. While the company has historically focused on organic growth, the consolidation within the fintech sector means that opportunities for synergistic acquisitions or strategic alliances may arise, allowing Axos to enter new markets or acquire new technologies and customer segments more rapidly.

The regulatory environment remains a significant consideration for any financial institution. Axos operates under the purview of various U.S. regulatory bodies, and compliance with evolving regulations is paramount. While compliance can represent a cost, it also serves to build trust and stability, which are essential for long-term customer loyalty and revenue generation. Changes in capital requirements, lending regulations, or consumer protection laws can all influence a bank’s operational capacity and profitability.

In summary, Axos Financial’s revenue outlook for fiscal year 2025 appears promising, driven by its successful digital banking strategy, diversified revenue streams, and adaptability to market dynamics. The company’s focus on technological innovation, operational efficiency, and strategic market positioning within the growing digital financial services landscape provides a solid foundation for continued financial success. While external economic forces and regulatory shifts will undoubtedly play a role, Axos’s inherent strengths suggest it is well-equipped to capitalize on the opportunities presented by the evolving financial services industry.