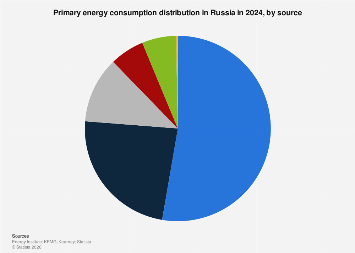

In 2024, Russia’s primary energy consumption landscape remained heavily anchored by natural gas, which secured the largest share of the nation’s energy mix. This dominant position underscores the country’s long-standing reliance on its vast hydrocarbon reserves, a cornerstone of both its domestic economy and its global energy influence. While precise figures are often subject to proprietary access, available analyses for the year indicate that natural gas accounted for a substantial portion of Russia’s total primary energy consumption.

Following closely behind natural gas was oil, historically another pillar of the Russian energy sector. Oil maintained its status as the second-largest contributor to the nation’s energy needs in 2024, reflecting its continued importance in transportation, industrial processes, and as a significant export commodity. The interplay between natural gas and oil consumption provides a clear picture of Russia’s energy priorities, heavily skewed towards fossil fuels.

Coal, while a significant energy source globally, occupied the third position in Russia’s primary energy consumption hierarchy for 2024. Despite its lower ranking compared to natural gas and oil, coal still played a crucial role, particularly in electricity generation and heavy industry. The relative shares of these three primary energy sources paint a picture of a mature energy market, deeply intertwined with the extraction and utilization of fossil fuels.

The composition of Russia’s energy consumption in 2024 is not merely a reflection of domestic demand but also a crucial element of its geopolitical strategy and economic resilience. As a leading global producer of oil and natural gas, Russia’s energy sector is intrinsically linked to international markets, with fluctuations in global energy prices and demand having a profound impact on its national revenue and economic stability. The year 2024, characterized by ongoing geopolitical realignments and a heightened focus on energy security worldwide, presented a complex environment for Russian energy policy.

Understanding the breakdown of Russia’s energy consumption provides critical insights into its industrial base, its export capabilities, and its vulnerability to external pressures. The significant share held by natural gas, for instance, points to the importance of its extensive pipeline infrastructure and its strategic role in supplying energy to both domestic consumers and international markets. The consistent demand for oil highlights its enduring significance in a global economy that, despite a growing push towards renewables, still heavily relies on petroleum products for a wide range of applications.

The data also implicitly suggests the challenges and opportunities facing Russia as it navigates the global energy transition. While the nation possesses abundant fossil fuel resources, there is increasing international pressure to decarbonize and a growing investment in renewable energy sources. The dominance of natural gas, often touted as a "bridge fuel" to a lower-carbon future, may offer Russia some strategic advantage in the short to medium term, but the long-term viability of such a heavily fossil fuel-dependent model remains a subject of considerable debate.

Globally, the trend in 2024 has been a complex mosaic of energy security concerns, price volatility, and a determined, albeit uneven, shift towards cleaner energy alternatives. Many nations are actively diversifying their energy portfolios, investing in solar, wind, and other renewable technologies, and exploring the potential of nuclear power. In this context, Russia’s continued reliance on natural gas and oil for the majority of its primary energy needs positions it differently from countries that are aggressively pursuing decarbonization targets.

The economic implications of this energy mix are far-reaching. Russia’s export revenues are heavily dependent on the global prices of oil and gas. Therefore, shifts in international demand, the development of alternative energy sources, and geopolitical events that disrupt supply chains can have significant ripple effects on the Russian economy. The robust domestic consumption of these fuels also underpins various industrial sectors, from manufacturing to agriculture, contributing to employment and economic activity.

Furthermore, the infrastructure associated with Russia’s energy sector – pipelines, refineries, power plants – represents a massive capital investment and a critical component of its national economic and security apparatus. Maintaining and upgrading this infrastructure, while also potentially investing in new, cleaner energy technologies, presents a significant financial and strategic challenge.

The relative share of coal in Russia’s energy consumption, though smaller than gas and oil, is still noteworthy. Coal remains a significant source of electricity generation in many parts of the world, and its continued use in Russia highlights the economic considerations and existing infrastructure that often dictate energy choices, especially in regions where alternative fuels may be less accessible or more expensive. However, the environmental implications of coal, including carbon emissions, are increasingly coming under scrutiny, and many countries are actively seeking to phase out its use.

In conclusion, the energy consumption patterns in Russia for 2024, with natural gas at the forefront, followed by oil and then coal, underscore a deep-seated reliance on fossil fuels. This configuration is a critical determinant of the nation’s economic performance, its geopolitical standing, and its engagement with the global energy transition. As the world continues to grapple with the complexities of energy security, climate change, and economic development, Russia’s energy landscape will undoubtedly remain a focal point of international analysis and strategic consideration. The balance between leveraging its abundant hydrocarbon resources and adapting to a rapidly evolving global energy paradigm will be a defining challenge for the nation in the years to come.