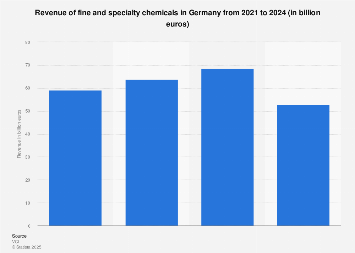

The German specialty chemicals market, a cornerstone of the nation’s industrial prowess and a significant contributor to its export economy, is projected to experience a notable revenue decline in 2024. This anticipated contraction, while not yet quantified with precise figures due to the proprietary nature of detailed market data, signals a challenging period for an industry renowned for its innovation and high-value products. Several interlocking factors, including subdued global economic activity, persistent inflationary pressures, evolving geopolitical landscapes, and a notable shift in demand patterns, are converging to create a less favorable operating environment for German chemical manufacturers.

Historically, Germany has held a dominant position in the global specialty chemicals arena. Its chemical industry, in general, is the largest in Europe and the fourth largest worldwide, with specialty chemicals representing a crucial segment characterized by bespoke formulations, high performance, and application-specific solutions. These chemicals are vital inputs for a vast array of downstream industries, from automotive and electronics to pharmaceuticals, agriculture, and construction. Their intricate production processes, intensive research and development (R&D) investments, and stringent quality controls have long cemented Germany’s reputation for excellence and reliability.

However, the current economic climate presents a stark contrast to the robust growth periods experienced in recent decades. The lingering effects of the COVID-19 pandemic, coupled with the ongoing energy crisis in Europe and broader global inflationary trends, have squeezed profit margins and dampened consumer and industrial spending. For the specialty chemicals sector, this translates into reduced demand from key end-use markets. For instance, the automotive sector, a significant consumer of specialty coatings, adhesives, and performance polymers, is navigating a complex transition towards electric vehicles, which, while offering future opportunities, is currently characterized by fluctuating production volumes and evolving material requirements. Similarly, the construction industry, a major buyer of specialty additives, sealants, and insulation materials, is facing headwinds from rising interest rates and slower housing market activity in many developed economies.

Furthermore, the globalized nature of the specialty chemicals market means that German producers are acutely sensitive to international economic fluctuations and trade dynamics. While the domestic market is substantial, a significant portion of German specialty chemical output is destined for export. A slowdown in major consuming regions, such as China, the United States, and other European nations, directly impacts the revenue streams of German companies. The increasing complexity of international trade relations, including tariffs and non-tariff barriers, adds another layer of uncertainty, compelling businesses to re-evaluate their supply chain strategies and market access.

The energy-intensive nature of chemical production also places German manufacturers at a disadvantage, particularly in light of elevated natural gas prices. While efforts are underway to diversify energy sources and enhance efficiency, the immediate impact of higher energy costs on production expenses is significant. This is especially pertinent for specialty chemicals, where complex multi-step synthesis processes can be particularly energy-demanding. Competitors in regions with lower energy costs or more stable supply chains may gain a competitive edge, potentially diverting market share away from German producers.

Despite these challenges, it is crucial to acknowledge the inherent resilience and innovative capacity of the German specialty chemicals industry. Companies operating in this sector are characterized by their strong commitment to R&D, often focusing on developing sustainable, high-performance solutions that address emerging global needs. The drive towards a circular economy, decarbonization, and digitalization presents new avenues for innovation. For example, the development of bio-based chemicals, advanced materials for renewable energy technologies, and sophisticated solutions for waste reduction and recycling are areas where German firms are well-positioned to lead.

The focus on sustainability, in particular, is becoming a critical differentiator. As regulatory frameworks worldwide increasingly emphasize environmental performance and product lifecycle assessments, companies that can offer greener alternatives and demonstrably reduce their environmental footprint are likely to gain favor with customers. This could involve investing in new production technologies, sourcing sustainable raw materials, or developing biodegradable or recyclable chemical products.

Looking ahead, the trajectory of the German specialty chemicals market in 2024 will likely be shaped by the interplay of these macroeconomic forces and the industry’s adaptive strategies. While a revenue contraction appears probable, the extent of this decline will depend on factors such as the pace of global economic recovery, the stabilization of energy markets, and the success of German companies in pivoting towards higher-growth segments and markets. The industry’s ability to leverage its R&D capabilities, embrace digital transformation, and capitalize on the growing demand for sustainable solutions will be paramount in navigating the current economic headwinds and positioning itself for future growth. The sector’s long-term prospects remain robust, underpinned by its foundational strengths in innovation, quality, and a deep understanding of complex chemical applications. However, the immediate future demands strategic agility, cost management, and a sharp focus on market opportunities that can withstand the current global economic uncertainties.