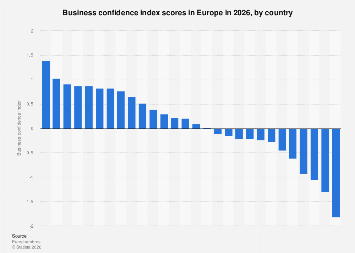

As the economic landscape of 2026 begins to take shape, a significant divergence in business sentiment is emerging across European nations, according to a comprehensive survey by the association of European chambers of commerce and industry. The findings reveal a clear stratification of optimism and pessimism, offering crucial insights into the perceived economic trajectory of individual countries and the continent as a whole. While some economies are poised for robust growth fueled by strong business confidence, others face a more subdued outlook, grappling with prevailing uncertainties.

At the apex of this business confidence index, three European countries stand out for their exceptionally positive outlook. Their business communities are demonstrating a pronounced optimism, suggesting a favorable environment for investment, expansion, and innovation heading into the new year. This high level of confidence is typically underpinned by a confluence of factors, including stable political environments, strong domestic demand, supportive regulatory frameworks, and promising export opportunities. For these nations, 2026 appears to be a year where businesses are prepared to take calculated risks and capitalize on emerging trends. The specific countries topping this optimistic list, though anonymized in the provided data, would likely exhibit strong indicators such as robust GDP growth projections, declining unemployment rates, and positive consumer spending trends in the preceding periods.

Conversely, the survey also identifies three European nations where business sentiment is notably more cautious, bordering on pessimistic. These countries are characterized by a business community that anticipates challenges and a less favorable economic climate. Factors contributing to this subdued outlook can range from persistent inflation and rising interest rates to geopolitical instability, supply chain disruptions, or internal economic structural issues. Businesses in these regions may be adopting a more defensive strategy, prioritizing cost containment and risk mitigation over aggressive expansion. Understanding the specific economic headwinds faced by these nations is crucial for policymakers seeking to foster a more balanced and resilient European economy.

The Eurochambres Business Confidence Index, as detailed in the supplementary notes, serves as a critical barometer for the economic health and future expectations of businesses across Europe. It is meticulously calculated by gauging the difference between the percentage of respondents reporting an expected "Increase" in their economic situation and those anticipating a "Decrease." This net balance is then further nuanced by considering the percentage of businesses expecting their situation to remain "Constant." This methodology allows for a nuanced understanding of sentiment, differentiating between outright optimism, outright pessimism, and a steady state of no change. A positive index value signifies a net optimistic outlook, while a negative value indicates prevailing pessimism. The magnitude of the index provides a quantitative measure of the intensity of this sentiment.

Delving deeper into the underlying economic drivers, the countries exhibiting high business confidence are likely benefiting from several key economic advantages. These might include a diversified industrial base, strong performance in key export sectors, a skilled and adaptable workforce, and effective fiscal and monetary policies that have fostered stability. For instance, countries with a strong manufacturing sector, particularly in high-value-added industries like advanced technology, pharmaceuticals, or automotive, often see their business communities projecting confidence when global demand for these goods remains robust. Furthermore, nations that have successfully navigated recent economic shocks, such as the energy crisis or post-pandemic recovery, with resilience are likely to see their businesses feeling more secure. The European Union’s commitment to digital and green transitions also presents significant opportunities, and countries at the forefront of these initiatives may be experiencing a corresponding boost in business confidence.

On the other hand, countries where business confidence is lagging may be contending with a more complex set of challenges. These could include an over-reliance on specific, volatile industries, ongoing labor shortages, high energy costs that haven’t been adequately addressed, or a perceived lack of clear government strategy for future economic development. The impact of global economic slowdowns, trade protectionism, or heightened geopolitical tensions can also disproportionately affect economies that are more exposed to international markets or are situated in regions experiencing heightened instability. For example, countries heavily reliant on tourism might still be recovering from the lingering effects of travel restrictions or shifts in consumer behavior. Similarly, nations with significant industrial sectors dependent on imported energy may continue to face cost pressures if long-term energy security solutions are not fully implemented.

The implications of these divergent confidence levels are far-reaching. For the optimistic nations, this sentiment can translate into increased capital expenditure, job creation, and a greater propensity for innovation. This can lead to a virtuous cycle of economic growth, attracting further domestic and foreign investment. Businesses are more likely to invest in research and development, expand their production capacity, and explore new markets, thereby contributing to a more dynamic and competitive economy. This proactive approach can solidify their position within the global marketplace and enhance their long-term economic resilience.

For the nations with lower business confidence, the outlook necessitates a more cautious approach. Businesses may scale back investment plans, delay hiring decisions, and focus on operational efficiencies to weather potential economic downturns. This can lead to slower economic growth, potentially higher unemployment, and a reduced capacity for innovation. It also signals a need for targeted policy interventions from national governments and potentially the broader European Union to address the specific concerns of these business communities. This could involve measures such as targeted fiscal support, regulatory reforms to reduce administrative burdens, investment in skills development, or initiatives to enhance energy security and diversification.

Comparing these trends on a continental scale, the overall picture for Europe in 2026 is one of mixed fortunes. While pockets of strong economic optimism offer hope, the persistent pessimism in other regions highlights the ongoing need for coordinated economic strategies and structural reforms across the continent. The European Union’s collective efforts to foster a more integrated and resilient single market, coupled with individual member states’ tailored approaches to domestic challenges, will be critical in navigating this complex economic environment. The ability of European businesses to adapt to evolving global dynamics, embrace technological advancements, and contribute to sustainable development will ultimately shape the continent’s economic trajectory in the years to come. The Eurochambres index, therefore, serves not just as a snapshot of current sentiment, but as a vital tool for forecasting economic performance and guiding policy decisions across a diverse and dynamic European economic landscape.