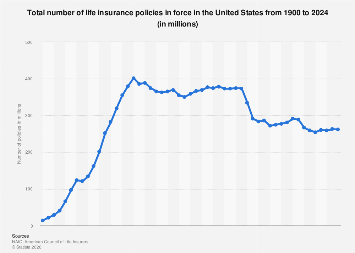

The landscape of life insurance coverage in the United States has experienced a prolonged period of plateau, with the total number of policies in force consistently hovering below a significant benchmark of 100 million since 2009. In the most recent data available for 2024, approximately 73 million life insurance policies were actively held by Americans, a figure that underscores a persistent, albeit less discussed, consequence of economic shifts on financial planning for households. This number represents a considerable segment of the population, yet it falls short of pre-2008 financial crisis levels, suggesting a lasting impact on consumer behavior and the perceived value of life insurance.

The reverberations of the 2008 global financial crisis cast a long shadow over the life insurance sector, with a noticeable decline in the number of active policies following the economic upheaval. In the immediate aftermath of the recession, the total number of life insurance policies in force saw a significant contraction, dropping from an estimated 77 million to approximately 70 million. This downturn illustrates a prevailing consumer sentiment during times of financial strain, where life insurance, often viewed as a discretionary expense rather than a foundational protection mechanism, becomes an early casualty of budget tightening. Even as the broader economy has demonstrated resilience and growth in the intervening years, the penetration of life insurance coverage has struggled to regain its pre-crisis momentum, indicating a potential recalibration of household financial priorities or a lingering erosion of confidence in its affordability or necessity.

While the sheer volume of policies has stagnated, a closer examination of the life insurance market reveals a more nuanced picture. The aggregate face value of individual life insurance policies, a measure reflecting the total death benefit coverage, has charted a consistent upward trajectory since 1998. This trend indicates that while the number of individual contracts may not be expanding significantly, those policies that are in force, or being purchased, are increasingly covering larger sums. This phenomenon could be attributed to several factors, including inflation-adjusted needs, increased awareness of the financial responsibilities associated with supporting dependents in a high-cost environment, and the growing complexity of estate planning for higher-net-worth individuals. Similarly, the total face amount of all life insurance policies, encompassing both individual and group coverage, has also exhibited a positive trend, mirroring the recovery observed in the individual policy market since the 2008 downturn.

Furthermore, the activity within the life insurance acquisition sphere offers a glimmer of positive movement. The number of new life insurance policy purchases appears to have reached a recent peak in 2023, suggesting a renewed interest or a more aggressive marketing and sales environment within the industry. This uptick in acquisition activity, even if it hasn’t immediately translated into a substantial increase in the total number of policies in force, signals that insurers are successfully engaging new customers. The drivers behind this surge in purchases could range from demographic shifts, such as a growing millennial and Gen Z population entering their prime earning and family-forming years, to targeted product innovation and more accessible distribution channels, including digital platforms.

Globally, the U.S. life insurance market, while substantial, faces similar challenges and opportunities as other developed economies. In many European nations, for instance, life insurance penetration rates can vary significantly, influenced by diverse social security systems, cultural attitudes towards financial planning, and prevailing interest rate environments. Countries with robust state-funded pension schemes might see lower individual demand for life insurance as a primary retirement savings vehicle, though its role as a death benefit protection remains crucial. Conversely, in rapidly developing Asian economies, the life insurance market is often characterized by high growth potential driven by rising disposable incomes, increasing urbanization, and a burgeoning middle class seeking financial security. The U.S. market, therefore, operates within a complex international context, where demographic trends, regulatory frameworks, and economic cycles all play a role in shaping consumer demand and industry performance.

The economic implications of this sustained plateau in policy numbers are multifaceted. For the life insurance industry itself, it suggests a need for strategic adaptation. Rather than solely focusing on acquiring new policyholders, insurers may need to prioritize customer retention, product innovation that appeals to evolving consumer needs, and exploring new revenue streams or service offerings. The focus on increasing the face value of policies, while positive for aggregate coverage, might not translate to proportional growth in the number of customers served, potentially impacting commission structures and the overall size of the insured population.

From a household financial security perspective, the sub-100-million mark for policies in force raises concerns about the preparedness of a significant portion of the American populace for unforeseen events. Life insurance serves as a critical financial safety net, providing funds for dependents to cover essential living expenses, mortgage payments, education costs, and other financial obligations in the event of the policyholder’s death. A lower number of policies, particularly among younger demographics or those with increasing financial responsibilities, could indicate a widening protection gap. This gap can lead to increased financial vulnerability for families, potentially exacerbating poverty and dependence on social welfare programs in the long term.

The insurance sector’s ability to demonstrate the value proposition of life insurance beyond its perceived cost is paramount. Educational initiatives, transparent communication about policy benefits, and tailored product offerings that address diverse life stages and financial goals are essential. The rise of InsurTech companies and digital platforms has opened new avenues for reaching consumers, simplifying the application process, and providing personalized advice. Leveraging these technological advancements can help bridge the information gap and make life insurance more accessible and understandable, potentially reversing the long-term stagnation in policy numbers.

Looking ahead, several macroeconomic factors will likely influence the trajectory of the U.S. life insurance market. Inflationary pressures, interest rate fluctuations, and the overall health of the labor market will continue to shape consumer purchasing power and their ability to allocate funds towards long-term financial products like life insurance. Demographic shifts, including an aging population and the increasing financial independence of women, will also present both challenges and opportunities for insurers. The industry’s capacity to adapt to these evolving dynamics, innovate its product offerings, and effectively communicate its indispensable role in financial planning will be critical in determining whether the number of life insurance policies in force can ascend to new heights or remain tethered to the levels seen in the post-recession era. The current data suggests a market that is mature, yet perhaps lacking the robust growth that signifies widespread financial preparedness.