The landscape of global finance has been profoundly shaped by the emergence and expansion of Sovereign Wealth Funds (SWFs), colossal investment vehicles established by governments to manage national reserves. While often associated with the oil-rich nations of the Middle East and Norway, the genesis and proliferation of these funds trace a longer, more intricate historical path, reflecting evolving economic philosophies, geopolitical shifts, and strategic diversification imperatives. Analyzing the establishment of SWFs over decades provides a compelling narrative of how nations have sought to harness their financial surpluses for long-term prosperity, intergenerational equity, and enhanced global economic influence.

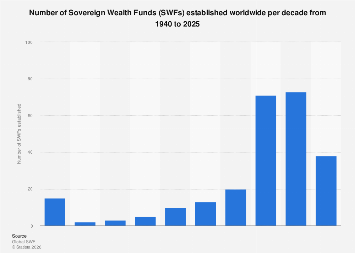

The earliest discernible precursors to modern SWFs began to take shape in the mid-20th century, albeit in nascent forms and with different motivations than today’s behemoths. The post-World War II era witnessed a surge in industrialization and economic development across many nations. For some, particularly those experiencing significant commodity booms, the accumulation of foreign exchange reserves became a strategic priority. Early examples, though not always explicitly labeled as SWFs, involved governments setting aside surplus revenues for future needs, often for infrastructure development or to stabilize national currencies. These were typically less sophisticated, often holding reserves in short-term government bonds or bank deposits, reflecting a primary focus on liquidity and capital preservation rather than active, diversified investment.

The 1960s and 1970s marked a period of increasing resource nationalism and a growing awareness of the long-term implications of commodity price volatility. Nations benefiting from burgeoning demand for oil, in particular, began to grapple with the challenge of managing substantial revenue windfalls. This era saw the formal establishment of some of the foundational SWFs, notably in Kuwait and Abu Dhabi, which were among the first to dedicate significant portions of their oil revenues to long-term investment strategies. The rationale was clear: to insulate national economies from the boom-and-bust cycles inherent in commodity markets and to build a sustainable financial legacy for future generations. These early funds, while growing rapidly, often operated with a degree of opacity, their investment strategies primarily focused on developed markets, seeking stable, income-generating assets.

The 1980s and 1990s witnessed a steady, albeit somewhat subdued, expansion in the SWF landscape. While major commodity exporters continued to build their reserves, other nations, particularly in Asia, began to establish funds as part of broader economic diversification strategies. The Asian Financial Crisis of the late 1990s, however, served as a stark reminder of the vulnerabilities associated with undiversified economies and fixed exchange rate regimes. This crisis catalyzed a re-evaluation of reserve management practices and provided a significant impetus for the creation and expansion of SWFs as tools for macroeconomic stability and strategic investment. Funds in countries like Singapore and South Korea, initially focused on currency management and foreign exchange reserves, began to evolve into more sophisticated investment entities.

The dawn of the 21st century heralded an era of unprecedented growth and diversification for SWFs. The commodity supercycle, driven by robust demand from emerging economies, particularly China, generated colossal revenues for resource-rich nations. This influx of capital fueled a dramatic expansion in the size and number of SWFs globally. By the early 2000s, SWFs were no longer confined to oil-producing states; they emerged in countries with significant trade surpluses, such as China, and even in developed nations seeking to manage pension liabilities or intergenerational wealth. The total assets under management by SWFs surged into the trillions of dollars, making them significant players in global capital markets. Investment strategies became more complex, encompassing a wider range of asset classes, including equities, real estate, infrastructure, private equity, and hedge funds. This period also saw a greater emphasis on transparency and governance, driven by international initiatives such as the Generally Accepted Principles and Practices for SWFs (Santiago Principles), which aimed to foster responsible investment and mitigate concerns about protectionism.

The period from 2010 to the present has been characterized by both continued growth and evolving challenges for SWFs. While many funds continued to accumulate assets, global economic volatility, geopolitical tensions, and the rise of protectionist sentiments introduced new complexities. SWFs have become increasingly strategic investors, seeking not only financial returns but also geopolitical influence, access to technology, and diversification away from traditional markets. Their investment mandates have broadened to include a greater focus on sustainable and responsible investing (ESG), reflecting growing global awareness of climate change and social impact. Furthermore, the sheer scale of SWF assets has made them crucial sources of capital for infrastructure projects, technological innovation, and cross-border mergers and acquisitions. However, their significant presence has also attracted scrutiny from regulators and policymakers concerned about national security implications, market manipulation, and unfair competition.

Looking ahead, the trajectory of SWFs is likely to be shaped by a confluence of factors. The global transition towards renewable energy will undoubtedly impact the revenues of traditional commodity-dependent funds, necessitating further diversification and adaptation of investment strategies. Geopolitical fragmentation and the potential for deglobalization could lead to increased regionalization of capital flows and a more cautious approach to cross-border investments. Moreover, the ongoing debate around the role of SWFs in national economies and global markets, particularly concerning their potential to distort competition or exert undue influence, will continue to shape regulatory frameworks and public perception. Despite these challenges, the fundamental rationale for SWFs – to prudently manage national wealth for long-term economic stability and prosperity – remains compelling. Their evolution from simple reserve managers to sophisticated global investors underscores their enduring significance in the international financial architecture, a significance that will continue to shape global capital markets and economic development for decades to come.