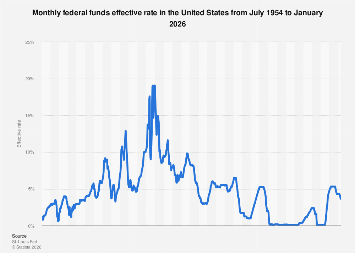

By late 2026, the Federal Reserve had decisively advanced its policy easing cycle, orchestrating a notable downward adjustment in the federal funds effective rate. This strategic shift marked the culmination of a multi-year trajectory that began with aggressive tightening and concluded with a sustained move towards more accommodative monetary policy. The year 2026 itself witnessed a continued reduction in borrowing costs, reflecting the central bank’s response to evolving economic conditions.

The journey to this point was a complex recalibration following an unprecedented period of monetary stimulus enacted in response to the COVID-19 pandemic. In the initial months of 2020, as the global economy reeled from the pandemic’s shockwaves, the Federal Reserve executed a rapid and substantial reduction in the federal funds rate. This benchmark rate, which dictates the cost for depository institutions to lend reserve balances to each other overnight, plummeted from a pre-pandemic level of approximately 1.50 percent in February 2020 to a historic low of near zero by March and April of the same year. These emergency cuts, implemented alongside a robust quantitative easing program, were crucial in stabilizing financial markets and injecting liquidity to prevent a deeper economic contraction.

For nearly two years, the federal funds rate remained anchored at this near-zero level, a stark contrast to the preceding decade. However, the persistent inflationary pressures that emerged in late 2021 and surged throughout 2022 necessitated a fundamental policy reversal. Beginning in early 2022, the Federal Reserve embarked on an aggressive tightening cycle, systematically raising the benchmark rate. This period of monetary restraint saw the federal funds rate climb from around 0.25 percent in April 2022 to a peak of approximately 5.50 percent by August 2023. This sustained period of elevated interest rates aimed to cool demand, curb inflation, and restore price stability.

After maintaining this restrictive stance for over a year, allowing the impact of rate hikes to permeate the economy, the Federal Reserve signaled a pivot. This shift began in September 2024, with the first rate cut of the cycle, reducing the federal funds rate to around 5.25 percent. This was followed by a further reduction to approximately 5.00 percent in December 2024, marking the initial phase of a broader policy recalibration that would extend through 2025 and into 2026.

Throughout 2025, the downward trend in the federal funds rate became more pronounced. Starting the year at an estimated 5.00 percent, the Federal Reserve implemented a rate cut in January, bringing the effective rate down. The rate remained stable for several months, reflecting careful observation of economic data. However, by September 2025, with inflation continuing to moderate and concerns about economic growth emerging, another reduction was enacted, lowering the rate to approximately 4.75 percent. Further easing occurred in the latter part of the year, with the rate being reduced to around 4.50 percent in November and then to an estimated 4.25 percent by December 2025. This sequence of actions underscored a clear commitment to a more accommodative monetary stance.

The easing trajectory continued unabated into 2026. By the close of 2026, the federal funds effective rate had settled at a significantly lower level, reflecting the Fed’s sustained efforts to stimulate economic activity and potentially respond to a more benign inflation environment. This phase of rate reductions has profound implications for various sectors of the U.S. economy. Lower interest rates typically translate into reduced borrowing costs for businesses, potentially spurring investment, expansion, and job creation. For consumers, this can mean more affordable mortgages, car loans, and credit card debt, potentially boosting spending and demand.

The Federal Reserve’s manipulation of the federal funds effective rate is a cornerstone of U.S. monetary policy, designed to influence broader economic variables. By adjusting this key rate, the central bank aims to steer economic growth, manage employment levels, and, crucially, control inflation. A lower federal funds rate generally encourages borrowing and spending, stimulating economic activity. Conversely, a higher rate discourages these activities, helping to curb inflationary pressures. The delicate balance the Fed attempts to strike involves fostering sustainable growth without igniting runaway inflation, or conversely, tightening policy too much and triggering a recession.

The Federal Reserve’s policy adjustments in the post-pandemic era were not conducted in a vacuum. They mirrored, to a significant extent, a globally synchronized monetary policy response. In the early stages of the pandemic, central banks worldwide, including the European Central Bank (ECB) and the Bank of England (BoE), also adopted aggressive easing measures. This global coordination aimed to cushion the economic blow and ensure the smooth functioning of international financial markets. For instance, major central banks collectively slashed their policy rates and expanded asset purchase programs.

As inflation became a more significant concern across developed economies starting in 2022, a synchronized tightening cycle ensued. Central banks across the globe raised interest rates to combat rising prices. However, as inflationary pressures began to recede in mid-2024, a global shift towards monetary easing became apparent. The Federal Reserve’s actions, therefore, were part of a broader international trend where central banks, having successfully navigated the peak of inflation, began to cautiously lower interest rates. This global easing trend, which broadened through 2025, indicated a collective assessment that the immediate inflation risks had diminished, and the focus was shifting towards supporting economic recovery and growth.

The impact of these policy shifts extends beyond domestic borders. As the Federal Reserve adjusts its rates, it influences global capital flows, currency exchange rates, and the cost of borrowing for international entities. A prolonged period of lower U.S. interest rates can make dollar-denominated debt cheaper for emerging markets, but it can also lead to capital outflows from these economies seeking higher returns elsewhere. Conversely, higher U.S. rates can attract foreign investment, strengthening the dollar but potentially increasing the debt burden for countries with dollar-denominated liabilities.

The sustained downward adjustment of the federal funds rate through 2026 suggests a Federal Reserve that anticipates a period of stable or moderating inflation, coupled with a potential need to support economic momentum. The effectiveness of this strategy will be closely monitored by markets, businesses, and policymakers alike, as it shapes the economic landscape for years to come. The journey from emergency stimulus to aggressive tightening, and now to a deliberate easing, highlights the dynamic and responsive nature of central banking in navigating complex and often unpredictable economic environments. The decisions made by the Federal Reserve, as reflected in the federal funds effective rate, continue to be a critical determinant of global economic health and stability.