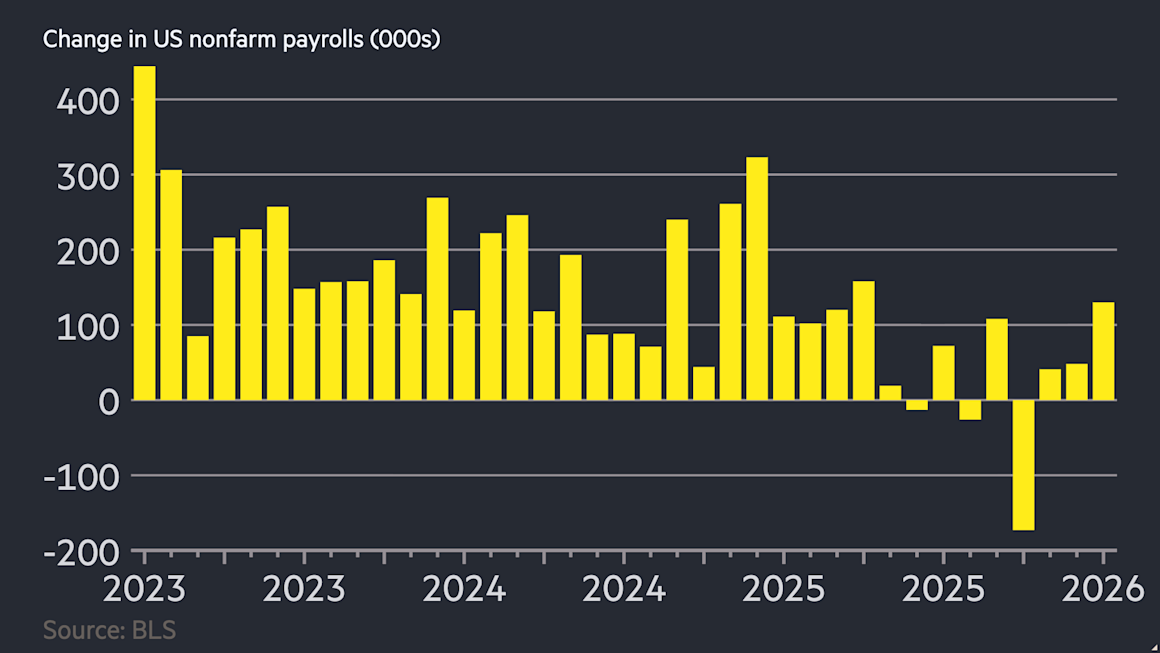

The American labor market demonstrated an unexpected level of durability at the start of the new year, adding 130,000 jobs in January and comfortably outpacing the more conservative estimates held by Wall Street economists. This latest data from the Bureau of Labor Statistics suggests that despite the prolonged period of elevated interest rates and the tightening of credit conditions, the underlying engine of the United States economy remains remarkably insulated from the broader global slowdown. While the headline figure of 130,000 positions might appear modest compared to the frantic hiring cycles seen in the immediate post-pandemic recovery, it represents a significant "beat" against a consensus that had braced for a sharper cooling of the employment engine.

This performance is particularly noteworthy given the context of the Federal Reserve’s ongoing battle against inflation. For much of the past two years, the central bank has maintained a restrictive monetary policy stance, aiming to dampen demand and bring the labor market into a more sustainable balance. The January report, however, indicates that the "soft landing" narrative—where inflation returns to the 2% target without triggering a recessionary spike in unemployment—remains a viable, if delicate, possibility. The resilience of the American worker continues to serve as the primary bulwark against the recessionary fears that have periodically gripped domestic markets.

Sector-level data reveals a nuanced picture of where this growth is concentrated. The services sector, which comprises the vast majority of the U.S. economy, continues to be the primary driver of headcount expansion. Healthcare and social assistance sectors showed particular strength, fueled by an aging demographic and a continued structural need for specialized care. Simultaneously, the leisure and hospitality industry, though no longer growing at its previous breakneck speed, contributed steady gains as consumer spending on experiences remains a priority for many households. Conversely, more interest-rate-sensitive sectors such as manufacturing and residential construction showed signs of a plateau, reflecting the higher cost of capital and a more cautious approach to long-term industrial expansion.

From a macroeconomic perspective, the January payroll beat complicates the Federal Reserve’s decision-making timeline. Investors and market participants have been eagerly scanning data for any sign of weakness that might justify a pivot toward interest rate cuts. However, a labor market that continues to add six-figure job totals monthly suggests that the economy is not yet in need of emergency stimulus. This "higher for longer" interest rate environment is likely to persist as long as the labor market remains tight enough to potentially fuel wage-push inflation. If businesses are forced to compete aggressively for a limited pool of talent, the resulting upward pressure on wages could eventually filter through to consumer prices, potentially stalling the progress made on the disinflationary front.

Average hourly earnings, a key metric for gauging inflationary pressure, are being monitored with renewed intensity following this report. While wage growth has moderated from its 2022 peaks, it remains at levels that many economists believe are inconsistent with a long-term 2% inflation target unless accompanied by a significant surge in productivity. The January data suggests that while the labor market is no longer "red hot," it is certainly not "cold." This "Goldilocks" scenario—not too fast to reignite inflation, but not too slow to signal a recession—is exactly what policymakers are aiming for, yet it leaves very little margin for error.

Global comparisons further highlight the unique position of the United States. While the Eurozone grapples with stagnation and the structural headwinds of high energy costs, and while China faces a complex recovery hampered by a property market crisis and demographic shifts, the U.S. consumer remains a global outlier in terms of spending power. This spending is directly supported by the security of a job market where the unemployment rate remains near historic lows. The "wealth effect" generated by a resilient stock market and stable housing values, combined with a steady paycheck, has allowed the American consumer to absorb the shocks of higher prices more effectively than their counterparts in other advanced economies.

Market reactions to the January jobs data were characterized by a reassessment of the "Fed pivot" timeline. Treasury yields edged higher as the probability of a March or May rate cut was recalibrated by futures traders. Equity markets showed a mixed response, balancing the positive news of a strong economy against the reality of prolonged high borrowing costs for corporations. For small and medium-sized enterprises (SMEs), which are more dependent on bank lending than their large-cap counterparts, the continued strength of the labor market is a double-edged sword: it ensures a steady stream of customers, but it also keeps the cost of servicing debt at levels that may limit their ability to invest in capital expenditures.

The labor force participation rate also remains a critical component of the broader economic story. Throughout the past year, an influx of workers—partially driven by the exhaustion of pandemic-era savings and a return to the workforce by older demographics—has helped to ease some of the labor shortages that plagued the 2021-2022 period. If the participation rate continues to hold steady or improve, it could allow the economy to continue adding 130,000 or more jobs per month without causing the labor market to overheat. This "supply-side" improvement is the ideal scenario for the Federal Reserve, as it expands the economy’s capacity without necessarily driving up prices.

However, risks remain on the horizon. The cumulative effect of monetary tightening often operates with a "long and variable lag." Some analysts warn that the 130,000 figure might be one of the last positive prints before the full weight of high interest rates finally catches up with the corporate sector. Large-scale layoffs in the technology and financial sectors, while localized so far, could eventually spill over into the broader economy if consumer confidence begins to waver. Furthermore, geopolitical tensions in the Middle East and the ongoing conflict in Ukraine continue to pose risks to global supply chains and energy prices, which could introduce new inflationary shocks that the Fed would be forced to counter with even more restrictive measures.

The January report also sheds light on the evolving nature of work in the post-pandemic era. The "Great Resignation" has transitioned into what some are calling the "Great Stay," as workers prioritize job security over the pursuit of marginal wage gains through frequent job-switching. This stabilization of the workforce is beneficial for employers in terms of reducing turnover costs and preserving institutional knowledge, but it also suggests a cooling of the entrepreneurial fervor that characterized the immediate post-2020 period. The 130,000 jobs added this month are more likely to be permanent, full-time roles in essential services rather than the speculative hiring seen in the tech boom of previous years.

In summary, the addition of 130,000 jobs in January serves as a testament to the underlying robustness of the U.S. economic framework. It challenges the prevailing gloom of those predicting an imminent downturn and provides the Federal Reserve with the breathing room to maintain its current policy stance until inflation is undeniably tamed. While the road ahead remains fraught with uncertainty—ranging from domestic political cycles to international trade disruptions—the start of the year has provided a solid foundation. The American labor market is not merely surviving the era of high interest rates; it is adapting to them, proving that the world’s largest economy possesses a level of flexibility that continues to surprise even the most seasoned market observers. As the year progresses, the focus will shift from whether the economy can create jobs to whether it can maintain this steady pace of growth without reigniting the inflationary fires that have proved so difficult to extinguish. For now, the January payroll figures offer a clear message: the American worker is still very much in demand, and the recession, for the time being, remains a distant prospect.