The European automotive market is undergoing a profound transformation, with electric vehicles (EVs) rapidly ascending to prominence. Projections for 2025 indicate a continued surge in EV adoption, with several models poised to dominate sales charts across the continent. This shift is not merely a trend but a fundamental recalibration of consumer preferences and regulatory imperatives, driven by a confluence of factors including ambitious emissions targets, evolving battery technology, expanding charging infrastructure, and increasing consumer awareness regarding environmental sustainability and long-term cost savings.

The European Union has set aggressive decarbonization goals, including a de facto ban on new internal combustion engine (ICE) vehicle sales from 2035. This legislative push acts as a powerful catalyst, compelling manufacturers to accelerate their electrification strategies and incentivizing consumers to make the transition sooner rather than later. As a result, the competitive landscape for EVs in Europe is intensifying, with established automakers and new entrants alike vying for market share. Data from industry analysts and market research firms suggests that by 2025, the top-selling EVs will likely represent a diverse range of vehicle types, from compact city cars to larger SUVs, reflecting the broadening appeal of electric mobility.

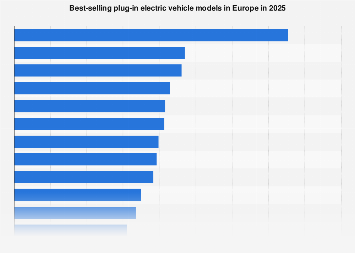

Several key players are expected to command significant portions of the European EV market. Volkswagen Group, with its comprehensive ID. family of electric vehicles, is a strong contender. Models such as the ID.3 and ID.4 have already established a solid foothold, and further iterations and new models are anticipated to bolster their sales figures. Similarly, Stellantis, formed by the merger of Fiat Chrysler Automobiles and PSA Group, is making substantial investments in electrification across its multiple brands, including Peugeot, Fiat, and Opel. Their commitment to launching a wave of new EV models, often built on shared modular platforms, positions them to capture a considerable share of the market.

The premium segment is also witnessing robust growth. Tesla, the pioneering force in the modern EV market, continues to be a dominant player with its Model 3 and Model Y. Their established brand recognition, advanced technology, and Supercharger network provide a distinct advantage. However, traditional luxury manufacturers are responding with formidable offerings. BMW’s iX and i4, Mercedes-Benz’s EQ range (such as the EQA, EQB, and EQS), and Audi’s e-tron models are all seeing increased demand, appealing to consumers who seek a blend of performance, luxury, and sustainability. The competition in this segment is particularly fierce, pushing innovation in areas like driving range, charging speed, and in-car technology.

Beyond these established giants, a host of other manufacturers are contributing to the vibrant European EV ecosystem. Hyundai and Kia have garnered significant praise and sales success with their innovative EV platforms, particularly the IONIQ 5 and EV6, which offer distinctive design and impressive performance. French manufacturers like Renault have long been active in the smaller EV segment with the Zoe, and are now expanding their electric offerings. Chinese manufacturers, such as BYD and MG (owned by SAIC Motor), are also making inroads, often leveraging competitive pricing and advanced battery technology to attract European buyers. Their growing presence underscores the globalization of the automotive supply chain and the increasing influence of Asian automakers in key Western markets.

Several factors contribute to the predicted success of these models. Firstly, the range anxiety that once plagued EV adoption is steadily diminishing as battery technology advances. Many new EVs now offer ranges exceeding 400-500 kilometers (approximately 250-310 miles) on a single charge, sufficient for the vast majority of daily commutes and even longer journeys. Secondly, the expansion of charging infrastructure across Europe is crucial. Governments and private entities are investing heavily in public charging stations, from rapid chargers along highways to slower chargers in urban areas and workplaces. This growing network significantly enhances the practicality of EV ownership.

Furthermore, the total cost of ownership for EVs is becoming increasingly attractive. While the initial purchase price can still be higher than comparable ICE vehicles, government incentives, lower electricity costs compared to fuel, and reduced maintenance requirements (due to fewer moving parts) often result in significant savings over the vehicle’s lifespan. Many European countries offer substantial subsidies, tax breaks, and other financial incentives for EV purchases, further sweetening the deal for consumers.

Market data supports these projections. In 2023, battery electric vehicles (BEVs) accounted for a significant and growing share of new car registrations across Europe. While specific figures for 2025 are forecasts, the upward trajectory is undeniable. For instance, data from the European Automobile Manufacturers’ Association (ACEA) has consistently shown double-digit growth in BEV sales year-on-year. Analysts predict that by 2025, BEVs could represent well over 20% of all new car sales in Europe, with some markets, particularly in Northern Europe, seeing even higher penetration rates.

The economic impact of this transition is far-reaching. It stimulates investment in battery manufacturing, charging technology, and renewable energy sources. It also presents challenges for traditional automotive supply chains and employment, necessitating reskilling and adaptation. The European automotive industry, a cornerstone of many national economies, is at the forefront of this industrial revolution, and the success of its electric offerings will be a key determinant of its future competitiveness on the global stage.

The competition is not limited to vehicle sales; it extends to technological innovation. Companies are investing heavily in areas such as solid-state batteries, faster charging capabilities, and advanced driver-assistance systems (ADAS) that can pave the way for autonomous driving. The integration of smart technologies, seamless connectivity, and intuitive user interfaces is also becoming a critical differentiator.

Looking ahead, the European EV market in 2025 will likely be characterized by intense competition, a widening array of attractive models, and an accelerating shift away from fossil fuel-powered vehicles. The success of specific models will depend not only on their technical specifications and pricing but also on their ability to resonate with European consumers’ growing environmental consciousness and their demand for sophisticated, sustainable transportation solutions. The ongoing evolution of policy, technology, and consumer behavior will continue to shape this dynamic and critically important sector of the global economy.