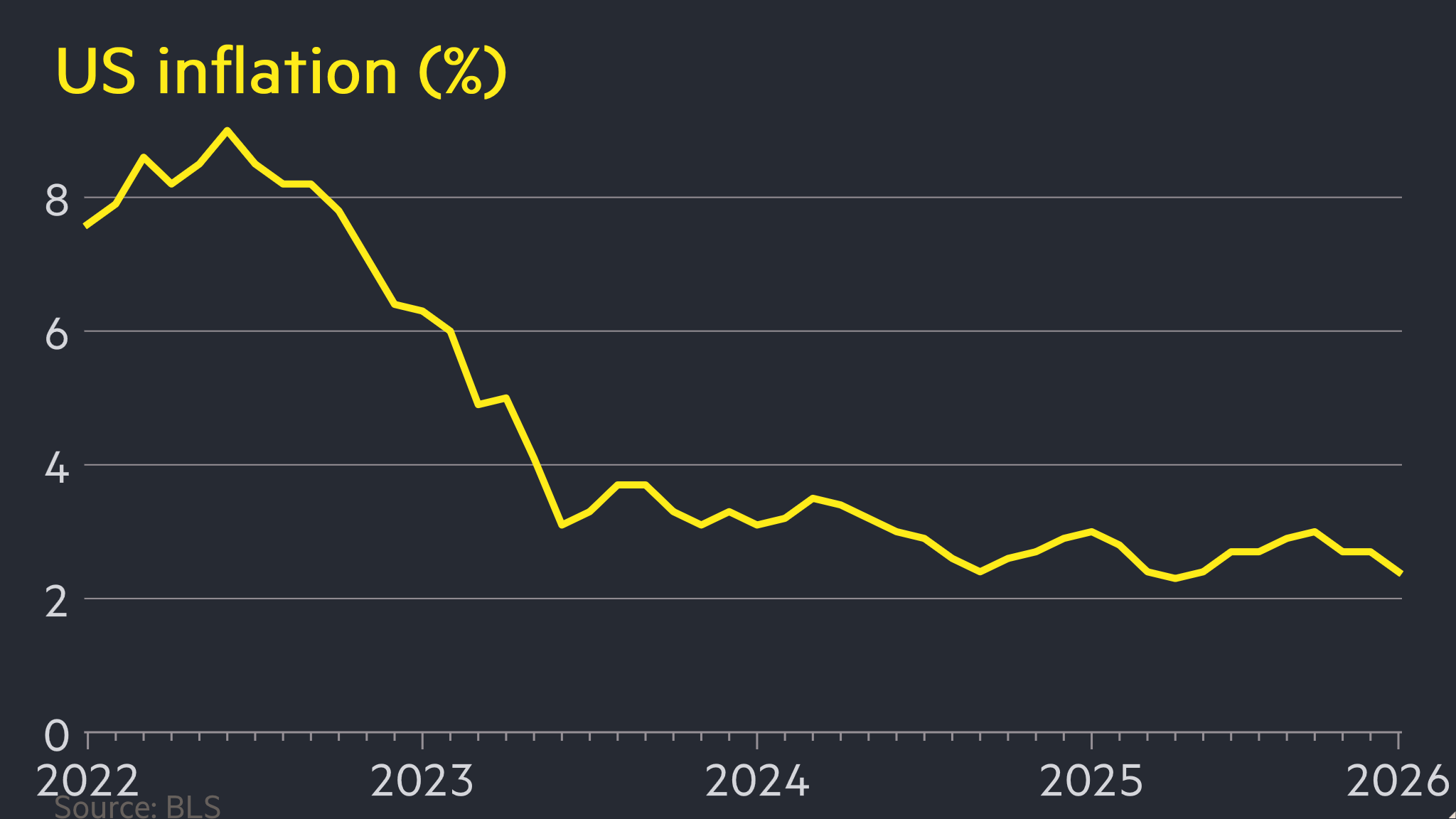

The trajectory of the American economy took a definitive turn toward stabilization this January, as the latest Consumer Price Index (CPI) data revealed a sharper-than-anticipated decline in inflationary pressures. According to the Bureau of Labor Statistics, the annual rate of inflation cooled to 2.4%, a figure that not only marks a significant retreat from the multi-decade highs seen in recent years but also suggests that the Federal Reserve’s aggressive monetary tightening cycle is yielding the desired results. This reading surpassed the consensus estimates of Wall Street economists, who had largely projected a more modest decline to 2.5% or 2.6%, sparking a wave of cautious optimism across global financial markets.

The descent to 2.4% represents a milestone in the post-pandemic economic recovery, signaling a return toward the price stability that characterized the decade preceding the 2020 global health crisis. For nearly two years, the Federal Open Market Committee (FOMC) has maintained a hawkish stance, elevating the federal funds rate to a 22-year high in a bid to dampen demand and anchor inflation expectations. The January data provides the strongest evidence yet that the "last mile" of the inflation fight—notoriously the most difficult phase of the disinflationary process—may be progressing more smoothly than skeptics had feared.

The internal mechanics of the January report highlight a broad-based cooling of prices, though certain sectors continue to exhibit residual stickiness. Energy prices played a pivotal role in the headline decline, as a combination of increased domestic production and a softening global demand outlook helped lower costs at the pump and reduced utility bills for American households. Food price appreciation also showed signs of exhaustion, with the "food at home" category reflecting a stabilization in supply chains that had been fractured by geopolitical tensions and climate-related disruptions over the past twenty-four months.

However, the "core" inflation metric, which excludes the volatile categories of food and energy, remains the primary focus for central bankers. While core inflation also edged lower, it continues to hover slightly above the headline figure, driven largely by the persistent costs of shelter and services. Housing remains a complex variable in the economic equation; because of the way the Bureau of Labor Statistics calculates "Owners’ Equivalent Rent," there is often a significant lag between real-time market rent decreases and their appearance in official government data. Analysts suggest that as the cooling rental market of late 2023 finally registers in the CPI, the shelter component will likely provide a further tailwind for disinflation in the coming quarters.

The labor market’s role in this disinflationary trend cannot be overstated. Traditionally, a rapid decline in inflation is accompanied by a spike in unemployment—a phenomenon described by the Phillips Curve. Yet, the current US economy appears to be defying historical precedents. January’s cooling inflation coincided with a labor market that remains robust, with unemployment figures hovering near historic lows and job creation continuing at a steady clip. This decoupling of high inflation from high employment is the hallmark of the elusive "soft landing," a scenario where the Federal Reserve manages to quell price surges without triggering a meaningful recession.

Wage growth, a critical driver of service-sector inflation, has also begun to moderate to levels more consistent with the Fed’s 2% long-term target. While workers are still seeing nominal gains, the frenetic pace of "the Great Resignation" has subsided, reducing the upward pressure on labor costs for businesses. This moderation allows companies to maintain margins without aggressively passing on costs to consumers, effectively breaking the dreaded wage-price spiral that haunted the US economy during the 1970s.

From a global perspective, the US performance in January stands in contrast to several other major economies. While the Eurozone and the United Kingdom have also seen inflation retreat from double-digit peaks, their progress has been slower, hampered by more acute energy vulnerabilities and structural labor shortages. The 2.4% figure places the United States at the forefront of the developed world’s disinflationary curve, potentially giving the Federal Reserve more flexibility than the European Central Bank or the Bank of England in the months ahead. Conversely, China continues to grapple with deflationary pressures, highlighting a fragmented global economic landscape where different regions are fighting vastly different monetary battles.

Financial markets reacted to the January data with a mixture of relief and recalibration. Treasury yields, which track interest rate expectations, saw a slight softening as traders increased bets that the Federal Reserve might initiate its first rate cut sooner than previously anticipated. Prior to this report, the "higher for longer" mantra dominated market sentiment, with many analysts pushing the first potential cut to the second half of the year. The 2.4% print has reopened the debate for a late spring or early summer adjustment, though Fed officials have remained steadfast in their messaging that they require "greater confidence" that inflation is sustainably on a path to 2%.

Jerome Powell, the Chair of the Federal Reserve, has frequently emphasized that the central bank is prepared to be patient. The memory of the 1970s, when the Fed cut rates too early only to see inflation roar back, looms large over the current leadership. Consequently, while the January data is a clear victory for the Fed’s strategy, it is unlikely to trigger an immediate pivot. Instead, it reinforces the transition from a period of active hiking to a period of "restrictive holding." The central bank is now in a data-dependent observation phase, weighing the risks of cutting too early (which could reignite inflation) against the risks of cutting too late (which could unnecessarily stifle economic growth).

Expert insights suggest that the "supercore" inflation—services excluding energy and housing—will be the final frontier for the Fed. This metric is more closely tied to domestic consumer demand and discretionary spending. As long as American consumers remain resilient, supported by high employment and rising real wages, the Fed may find that the final 0.4% gap between current levels and their 2% target is the most stubborn to bridge. There is also the looming shadow of geopolitical risk; should tensions in the Middle East or Eastern Europe escalate further, disruptions to maritime trade routes or global oil supplies could easily inject a fresh dose of volatility into the commodity markets, reversing the gains made in January.

The economic impact of 2.4% inflation extends beyond the halls of the Federal Reserve and into the everyday lives of the American public. After years of seeing their purchasing power eroded, consumers are finally experiencing a period where wage growth is outpacing price growth in real terms. This shift is critical for consumer sentiment, which has lagged behind other economic indicators. If the trend of moderating prices continues, it could bolster domestic consumption—the engine of roughly two-thirds of the US economy—and provide a stable foundation for corporate investment in 2024.

As the year progresses, the focus will shift from the headline number to the sustainability of this trend. The Federal Reserve’s preferred gauge, the Personal Consumption Expenditures (PCE) price index, typically runs slightly lower than the CPI, meaning the Fed’s target may be even closer than the 2.4% CPI figure suggests. However, the path to 2% is rarely a straight line. Economic data is inherently "noisy," and seasonal adjustments in the early months of the year can sometimes distort the underlying reality.

Ultimately, the January inflation report serves as a powerful validation of the current economic trajectory. It suggests that the United States is navigating a unique historical moment where massive fiscal stimulus and rapid monetary tightening have balanced out without the catastrophic "hard landing" that many predicted a year ago. While the mission is not yet fully accomplished, the retreat to 2.4% provides a clear signal that the era of rampant price instability is nearing its end, allowing businesses and households to plan for a more predictable and prosperous future. The eyes of the global financial community will now remain fixed on the Fed’s next move, as it decides when and how to begin easing the restrictive measures that helped bring the economy to this pivotal juncture.