On election night in November 2024, a wave of optimism swept through the United States’ cryptocurrency industry, fueled by the prospect of the first unequivocally crypto-friendly administration in American history. Bitcoin surged to an unprecedented high of over $75,000, and crypto-related equities experienced a significant rally. Donald Trump, who had declared on the campaign trail his desire for America to "mine, mint, and make" the future of digital money, was widely hailed as a leader wholeheartedly embracing this nascent sector. This sentiment proved prescient.

Just months into his second term, President Trump enacted the "Guiding and Establishing National Innovation for US Stablecoins Act," colloquially known as the GENIUS Act. This landmark legislation established the first comprehensive federal framework for stablecoins – digital tokens pegged to the U.S. dollar that serve as the foundational currency of the cryptocurrency economy. The Act represents a pivotal moment for digital money, signaling both immense opportunity and inherent risks.

Private Innovation Meets Public Scrutiny

The GENIUS Act mandates stringent regulations for issuers of dollar-backed digital tokens. These requirements include maintaining full, verifiable reserves in cash or short-term government bonds, submitting to monthly attestations of these holdings, adhering to clear redemption obligations, and complying with anti-money laundering and consumer protection rules. Critically, the legislation classifies stablecoins as payment instruments rather than securities, thereby resolving years of regulatory ambiguity and mitigating litigation risks for issuers. "We are witnessing a shift of stablecoins from simply being ‘crypto’ or ‘digital currency’ to being core payments infrastructure," observes Mike Hudack, co-founder of Sling Money, a crypto-enabled money transfer application that utilizes stablecoins.

Beneath the surface of industry exuberance lies a profound strategic calculation. The Act represents not only an embrace of innovation but also a deliberate alternative to a central bank digital currency (CBDC). One of President Trump’s earliest actions in his second term was to prohibit U.S. authorities from issuing a digital dollar. By rejecting a government-controlled digital dollar, a project largely associated with the previous administration, Washington effectively delegated the future of digital money to the private sector. This decision reflects a complex interplay of ideology, market pragmatism, and political strategy. White House officials argued that a digital dollar would have placed the government too intimately within citizens’ financial lives, raising concerns about financial surveillance. In contrast, stablecoins offer a market-driven model for digital payments, aiming to preserve the dollar’s global dominance and maintain U.S. financial hegemony in an increasingly digitized world. Currently, approximately 99% of all stablecoins are denominated in U.S. dollars, meaning each transaction reinforces the greenback’s international reach.

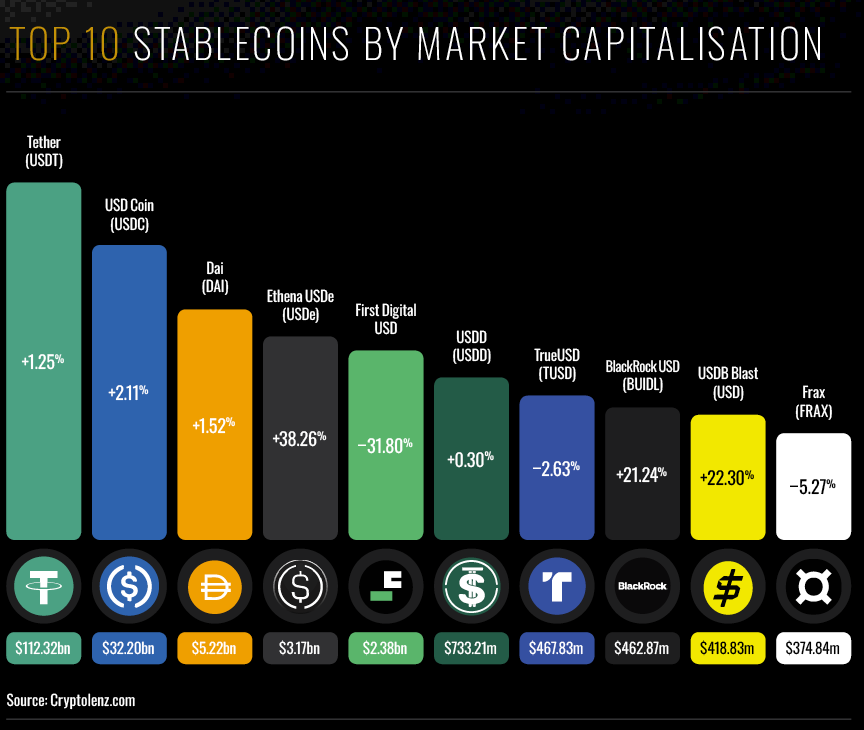

This choice also aligns with the administration’s ideological aversion to expanding federal control over money, a stance that resonated with both libertarians and the business community during the campaign. "A CBDC would concentrate financial power within the government, something this administration was never likely to endorse," explains Maghnus Mareneck, co-CEO of Cosmos Labs, a U.S. blockchain firm that develops interoperability protocols used by financial institutions. "The administration recognizes that stablecoins can modernize the dollar without replacing it." The legislation was met with widespread enthusiasm from cryptocurrency firms, which had long chafed under years of regulatory uncertainty. Many argued that the Securities and Exchange Commission (SEC), under its previous leadership, had stifled the industry through aggressive regulatory actions. During his campaign, Trump had pledged to replace Gary Gensler, the SEC chairman appointed by the Biden administration who had been a key figure in shaping crypto regulation. Gensler’s departure in January, ahead of his term’s scheduled end in 2026, paved the way for a significant shift in the agency’s regulatory philosophy. In the months following the GENIUS Act’s passage, the stablecoin market experienced explosive growth. Once a niche segment, total stablecoin capitalization surpassed $300 billion by October, expanding at twice the pace of the broader crypto sector. Analysts at Citi project this market could reach $4 trillion by 2030. Tether, the leading issuer of dollar-based stablecoins, is reportedly seeking up to $20 billion in new capital, a move that would elevate its valuation towards the $500 billion mark.

However, critics have voiced concerns about the Act’s relatively lenient approach to the inherent risks associated with stablecoins. "What the Act does is vastly expand the network effects that make it easier to launder money and operate in the underground economy. It is important for the government to be able to monitor and audit transactions, and the bill is very light on that," states Professor Kenneth Rogoff, an international economics professor at Harvard University and former Chief Economist of the International Monetary Fund (IMF). David Hoppe, founder of Gamma Law, a U.S. firm specializing in digital asset cases, points out that the Act "does not guarantee timely redemption or provide federal insurance, and it lacks clear rules for dispute resolution, unauthorized transfers, or fraud recovery. Oversight is fragmented across state and federal channels, creating space for inconsistent enforcement and charter shopping."

Banks on Guard: Opportunity and Existential Threat

For the traditional banking sector, the rise of state-sanctioned stablecoins presents a dual challenge: both significant opportunity and potential existential risk, primarily through disintermediation. While few stablecoins currently offer interest, the prospect of issuers beginning to provide yield, coupled with widespread business adoption for payroll, trade, and settlements, could lead to substantial deposit outflows from banks. This would weaken their traditional deposit-funded lending models and imperil credit creation capabilities. Their balance sheets, already facing pressure from digital payment platforms, could contract further. A recent U.S. Treasury report estimates that up to $6.6 trillion in deposits could leave bank coffers if crypto exchanges are permitted to offer interest payments or similar financial incentives, a scenario U.S. banks are actively lobbying policymakers to prevent.

Legacy lenders are adopting a cautious stance, recognizing their enduring advantages. "If banks issue their own stablecoins directly, they would be safer, because they have direct access to central bank reserves," notes Lucrezia Reichlin, an economist at the London Business School. Major financial institutions like JPMorgan Chase and Citi are actively exploring the issuance of their own dollar-pegged payment tokens. In Europe, nine financial institutions, including UniCredit and ING, are developing euro-denominated stablecoins. "Banks may look to position themselves as the infrastructure and control layer for stablecoin custody, settlement, and on-chain treasury, providing KYC, segregation, and policy controls, so they can capture fee revenue as liquidity and payments migrate on-chain," suggests Susana Esteban, Managing Director of the Blockchain and Digital Assets practice at FTI Consulting. Their ultimate goal, she adds, could be the offering of tokenized deposits, providing the same "24/7, programmable experience" that stablecoins promise.

The implications extend beyond mere transactional efficiency to encompass financial sovereignty. The expanding role of privately issued dollar tokens could diminish the influence of many central banks, fundamentally altering the architecture of international finance. "Stablecoins do not create base currency, so they don’t directly erode the Federal Reserve’s ability to set short-term rates or influence market liquidity," states Jonathan Church of TransferMate, a fintech payments infrastructure firm. However, central bankers express concern that a widespread migration to stablecoins could reduce their control over money creation and interest rate transmission, forcing monetary policy to operate through less predictable channels. As a greater volume of money circulates outside the regulated banking system, the transmission of interest rate adjustments to the broader economy could become slower and less certain. Andrew Bailey, Governor of the Bank of England, has recently warned that stablecoins could "separate money from credit provision," as non-bank entities assume a more significant role in financial intermediation.

The international payments group Swift is also actively adapting, collaborating with major banks like Bank of America, Citi, and NatWest to develop a shared blockchain ledger designed to facilitate transactions, particularly the settlement of tokenized assets, including stablecoins. The emergence of stablecoins poses a direct challenge to Swift’s traditional role by enabling instantaneous transfers that bypass established intermediaries. Transactions that once took several days and involved multiple compliance checks can now be executed in seconds, disrupting decades of built financial infrastructure. Swift’s strategic adjustments serve as a microcosm for the broader financial system’s imperative: in an era of programmable, borderless money, legacy institutions must evolve or risk becoming obsolete.

The Trump Effect and Geopolitical Undercurrents

As with many aspects of the Trump presidency, the line between public policy and private interest appears blurred. Members of the President’s family have launched ventures in the crypto space, including World Liberty Financial, the issuer of the USD1 stablecoin, and American Bitcoin, a mining company co-founded by Donald Trump Jr. and Eric Trump. A meme-token, $TRUMP, bears the President’s name. This intermingling of political and commercial interests is not unprecedented for this administration, but the stakes are significantly higher. Unlike traditional businesses like hotels or golf courses, stablecoins touch the very foundations of the global financial system.

For supporters, the symbolism is powerful: the self-proclaimed deal-maker, once renowned for building skyscrapers, now aims to anchor American influence in the realm of digital money. Critics, however, contend that this alignment of public policy with private profit risks eroding confidence in the neutrality of U.S. financial regulation. Lawmakers and ethics experts have called for enhanced safeguards, including restrictions on digital asset ownership by politicians and senior officials, and more robust blind-trust requirements. "The president directs agencies responsible for implementing the Act, while his family benefits from a company whose success depends on those same regulations," notes Gamma Law’s David Hoppe. "Even if lawful, such circumstances create the perception that private gain could influence public policy, which risks undermining confidence in fair enforcement and market integrity."

For the moment, the administration appears unfazed. Within Washington’s strategic calculus, the digital future of money must remain denominated in dollars, even if those dollars are minted by private entities. In this context, the GENIUS Act can be viewed as a geopolitical statement. Both administration officials and members of the Trump family frame the policy as a direct response to de-dollarization efforts spearheaded by China. "Crypto is actually going to be the thing that preserves dollar hegemony around the world," stated Donald Trump Jr. at a recent crypto conference in Singapore. He added, "As stablecoins start becoming the markets and treasuries, that’s going to replace China and Japan and some of these places that say, ‘You know what? We don’t want America to have that power anymore.’"

China’s Digital Yuan Gambit and Europe’s Response

One of China’s strategies to challenge dollar dominance is the accelerated rollout of its central bank digital currency (CBDC), the digital yuan. This initiative gained further momentum following international sanctions against Russia, which implicated Chinese banks accused of facilitating the procurement of weapons parts for Moscow. Beijing has also actively promoted its Cross-Border Interbank Payment System (CIPS) and seen a dramatic increase in overseas lending denominated in renminbi, with outbound renminbi loans, deposits, and bond investments by Chinese banks quadrupling since 2020. Furthermore, China is a key driver behind the m-CBDC Bridge, a multi-CBDC platform designed to facilitate cross-border payments, governed by the central banks of China, Hong Kong, Thailand, Saudi Arabia, and the United Arab Emirates.

"China’s ambition is not to replace the dollar or make the yuan an alternative to it. They know that it would be unrealistic," observes Lucrezia Reichlin, the London Business School economist. "But they want to defend the payment system in their financial ecosystem and one way to do it is to control the rails for cross-border payments via digital solutions."

China approaches stablecoins with significantly more caution. Last summer, the Hong Kong Monetary Authority began accepting applications from stablecoin issuers, a move widely interpreted as Beijing’s response to the U.S. GENIUS Act. Chinese officials suggested that China should counter the U.S. promotion of stablecoins by developing a renminbi-pegged stablecoin to boost the yuan’s international usage. However, since then, various Chinese regulators, including the People’s Bank of China, have expressed reservations about yuan-based stablecoins, citing concerns that private stablecoins could undermine the development and adoption of the digital yuan. This regulatory scrutiny has prompted major Chinese tech firms such as Ant Group and e-commerce group JD.com, which were expected to participate in Hong Kong’s pilot program, to postpone their stablecoin issuance plans. "Beijing wants every digital yuan transaction, whether it is domestic or international, to move through systems it can oversee. Stablecoins inherently create alternative payment networks that the state cannot easily legislate, and that introduces risk and potential fragmentation of issuance for this government," explains Mareneck of Cosmos Labs, an expert on Asian stablecoins.

The U.S. push for stablecoin supremacy has also prompted concern among European policymakers and the European Central Bank (ECB), which is progressing with its own digital euro project. Despite being the first major economic bloc to establish a comprehensive stablecoin regulatory framework with its Markets in Crypto Assets (MiCA) regulation, Europe currently does not prioritize stablecoins. Experts warn that Europe risks repeating past mistakes by over-regulating a nascent market, potentially allowing American platforms to dominate it. "MiCA has a number of restrictions, and many in Europe appear to be focused on protecting banks rather than embracing technological innovation. Stablecoins enable easy access to U.S. short-term government bonds from all parts of the world, which also diverts capital flows from the EU and the UK to the U.S.," notes Gilles Chemla, a finance professor at Imperial Business School. Concerns over sovereignty are a primary driver of the EU’s CBDC program, as it seeks to reduce reliance on U.S. payment giants like Visa and Mastercard.

However, experts question the feasibility of this goal if dollar-denominated stablecoins become widely adopted in Europe, and whether a digital euro is the most effective tool to achieve this objective. "The digital euro in its current design is narrowly focused on the euro area as a means of payment only for private households and with holdings limited to €3,000, while stablecoins offer an international payment scheme that can be used by global companies," argues Peter Bofinger, an economist at Würzburg University and a former member of the influential German Council of Economic Experts. Bofinger suggests that a more effective approach for the EU would be the integration of its existing national payment systems.

Should dollar-backed stablecoins gain significant public adoption within the Eurozone, the ECB will face difficult choices. "There is a risk of dollarization. Dollar-backed stablecoins could become what the eurodollar market is now: a big offshore dollar-based market," warns Reichlin, the London Business School economist and former ECB director general of research. "If Europe doesn’t develop euro-pegged stablecoins, the old payment system could be dollarized, especially large cross-border payments. Europe is complacent about this risk." Conversely, some analysts believe warnings about dollarization are overstated. "The ECB is raising the risk of dollarization to justify the need for a digital euro," states Bofinger. "There’s no such risk, because currencies are like languages: to switch from a domestic currency to a foreign one, the domestic currency has to be in a terrible state, like in some Latin American countries."

Another concern for the ECB is that dollar-backed stablecoins could diminish the euro’s global standing. Their widespread adoption in Europe might also weaken the ECB’s control over monetary policy. "Every tokenized dollar transaction strengthens the dollar’s global position, even beyond U.S. borders. A euro CBDC cannot match that momentum, and will likely be slower, more limited, and less compatible with global blockchain systems," says Mareneck of Cosmos Labs. Reichlin adds, "It was a mistake of the ECB to think of CBDCs as an alternative to private stablecoins. These are two different things. CBDC is similar and complementary to cash, whereas stablecoin is complementary to deposits. There is no reason why CBDCs and stablecoins could not coexist."

The Shadow Banking Risk and Speculative Bubbles

Nearly two decades after the 2008 credit crunch, policymakers remain acutely aware of its lingering effects. Stablecoins are expected to be backed by safe, liquid assets, and users should be able to redeem them at par. "Because stablecoins are not lent out the way bank deposits are, you can argue that in some respects they are likely to be at lower risk than bank deposits, though governments are more likely to bail out banks than stablecoin companies," suggests Paul Brody, a blockchain expert at Ernst & Young. However, economists caution that stablecoin issuers effectively operate as shadow banks, but without the same capital requirements, access to central bank liquidity, or regulatory oversight. A loss of confidence in their reserves could trigger cascading effects into bond markets and precipitate liquidity crises, echoing the panics of 2008 and 2020, and potentially forcing governments into politically challenging bailouts. "If a major stablecoin issuer is unable to meet redemptions or discloses reserve weaknesses, trust could unravel quickly, prompting mass withdrawals. The impact would extend beyond digital assets, affecting wider financial markets that rely on tokenized instruments for settlement and liquidity," states Krishna Subramanyan, CEO of Bruc Bond, a cross-border banking and payments provider.

A significant concern is that speculation could once again overshadow regulatory caution. Although the GENIUS Act prohibits the issuance of interest-bearing stablecoins, it does not explicitly forbid third parties from offering interest-bearing financial products that involve stablecoins. Experts warn that the creation of such reward-based products could foster a parallel deposit market that competes on yield with only a tenuous guarantee of one-to-one convertibility, thereby complicating monetary control. "Because stablecoins are vulnerable to runs, a fire sale of their reserve assets – such as bank deposits and government debt – could spill over into bank deposit markets, government bond markets, and repo markets," the IMF warned in a recent financial stability report. Susana Esteban from FTI Consulting proposes, "A practical safeguard is integration rather than prohibition: preserve monetary control by including stablecoin flows in the liquidity toolkit using facilities such as the Standing Repo Facility and Reverse Repo Facility to absorb shocks while supervisors treat major issuers as systemically important payment institutions subject to stress testing and live disclosure."

Security remains a critical consideration. Some experts caution that, similar to other forms of cryptocurrency, stablecoins could be exploited for illicit activities such as money laundering and are susceptible to cyberattacks and technical glitches. Stablecoin issuers may need to secure insurance to reimburse holders in the event of cyberattacks and to cover operational risks, which would inevitably increase their costs. Political uncertainty could also fuel volatility; a future Democratic administration might impose more stringent regulations on stablecoins. "Expect a revisit of the CBDC ban, stricter consumer protections, and tighter perimeter rules for issuers regarding resolution, interoperability, and wallet safeguards," predicts Maja Vujinovic, CEO of Digital Assets at FG Nexus.

By the time of the next presidential election, America’s financial experiment with stablecoins may have grown too substantial to fail. The wager is audacious: that the profit motive of dollar-denominated token issuers will align seamlessly with national interests. In this sense, the GENIUS Act embodies a paradox: it aims to enhance dollar supremacy while simultaneously diminishing Washington’s direct control over money creation. Can this hybrid model of monetary sovereignty – one where Wall Street and Silicon Valley, rather than the Federal Reserve, wield significant influence over global finance – live up to the expectations of crypto enthusiasts and the Trump administration, or will it sow the seeds of the next financial crisis? The answer hinges on the enduring forces that have long shaped finance: confidence, liquidity, and the unwavering belief that the system, despite its imperfections, will ultimately hold.