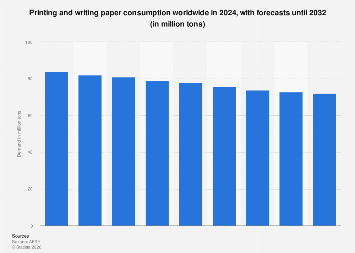

The worldwide demand for printing and writing paper is set to contract significantly over the coming decade, a trend driven by a confluence of digital transformation, evolving consumer habits, and economic pressures. In 2024, global consumption stood at an estimated 84 million tons. Projections indicate a steady downward trajectory, with demand anticipated to reach 72 million tons by 2032. This represents a substantial decrease, underscoring a fundamental shift in the paper industry’s most traditional segments.

This projected decline is not an isolated incident but rather a continuation of a longer-term pattern. Global graphics paper production, a key component of the printing and writing paper market, has already experienced a notable downturn. Between 2010 and 2024, production in this sector fell by more than 40 percent, signaling the profound impact of digital alternatives on paper-based communication and information dissemination. The data for the period 2024-2032, which includes forecasts from the current year onward, paints a stark picture of diminishing market share for these products.

The year-over-year figures illustrate this contraction clearly. After the 84 million tons consumed in 2024, demand is expected to fall to 82 million tons in 2025, followed by 81 million tons in 2026. The pace of decline is projected to continue, with consumption expected to be 79 million tons in 2027, 78 million tons in 2028, 76 million tons in 2029, 74 million tons in 2030, 73 million tons in 2031, and finally reaching 72 million tons in 2032. This consistent year-on-year reduction highlights the pervasive nature of the challenges facing the sector.

Several interwoven factors are contributing to this market contraction. The most significant driver is the accelerating digital revolution. Businesses and consumers alike have increasingly adopted digital platforms for communication, documentation, and entertainment. Emails, e-books, online publications, and digital marketing campaigns have steadily replaced their paper-based counterparts. This shift is particularly pronounced in developed economies, where internet penetration and access to digital devices are widespread. The convenience, cost-effectiveness, and environmental considerations associated with digital formats have made them the preferred choice for a growing proportion of the global population.

Furthermore, the COVID-19 pandemic, while not explicitly factored into the provided figures, likely exacerbated this trend. The surge in remote work and online learning necessitated a rapid adaptation to digital tools, further entrenching digital habits. While some sectors may see a partial rebound as the world adapts to a post-pandemic reality, the long-term impact on paper consumption is expected to remain negative. The supplementary notes accompanying the data mention that the figures do not consider COVID-19’s potential impacts, suggesting that the actual decline could be even more pronounced than currently forecast.

The economic implications of this decline are far-reaching for the paper industry. Manufacturers are facing declining revenues and profits, necessitating strategic adjustments. This includes diversifying product portfolios, investing in sustainable practices and alternative fiber sources, and exploring new markets. The industry is also grappling with the need to optimize production processes, reduce costs, and enhance operational efficiency to remain competitive. Some companies may choose to exit the printing and writing paper segment altogether, focusing on more resilient sectors like packaging or specialty papers.

The global geographical distribution of this trend is also noteworthy. While developed markets in North America and Europe are likely to experience the most significant contractions due to advanced digital infrastructure, emerging economies in Asia and Africa might show a more varied response. In regions with lower digital penetration, the demand for printing and writing paper might remain more resilient for a longer period, driven by increasing literacy rates and growing access to education and commerce. However, even in these markets, the long-term shift towards digital is inevitable as technological adoption accelerates.

Industry experts have long been sounding the alarm about the structural changes occurring within the paper sector. Dr. Anya Sharma, a senior analyst at Global Paper Insights, commented, "The printing and writing paper market has been in a state of secular decline for years, and the digital transformation has only accelerated this process. Companies that fail to adapt their business models, focusing on niche markets, sustainable solutions, or value-added products, will struggle to survive." She further emphasized the importance of innovation, stating, "The future for paper lies not in mass production for general printing, but in specialized applications, intelligent packaging, and products derived from sustainable forestry practices."

The decline in printing and writing paper demand also has environmental implications. While a reduction in paper consumption can be seen as positive from a sustainability perspective, reducing deforestation and carbon emissions, the paper industry is also a significant employer and economic contributor in many regions. The transition needs to be managed carefully to mitigate job losses and economic disruption. Investment in green technologies and the development of a circular economy for paper products will be crucial in navigating this shift.

Moreover, the broader economic context plays a vital role. Global economic slowdowns, inflation, and geopolitical instability can further impact consumer spending and business investment, including the demand for paper products. Businesses may reduce their spending on marketing materials and internal documentation, while consumers may cut back on discretionary purchases of printed matter.

The data also highlights a discrepancy in the reported figures, with supplementary notes indicating that "the figures in the statistics differ from the ones published by the source due to a probable misprint in the most recent edition of the report." This suggests a need for caution and further verification of the exact figures, although the overall trend of decline remains consistent and widely acknowledged by industry observers.

In conclusion, the global printing and writing paper market is facing a challenging decade ahead. The persistent shift towards digital alternatives, coupled with evolving consumer preferences and economic headwinds, points towards a sustained period of contraction. The industry’s ability to adapt through innovation, diversification, and a commitment to sustainability will determine its long-term viability in an increasingly digitized world. The projected decrease from 84 million tons in 2024 to 72 million tons by 2032 is a clear indicator of the significant transformation underway, necessitating strategic foresight and proactive adaptation from all stakeholders.