The European cloud computing market in 2024 is characterized by a dynamic interplay of established giants and emerging players, with market share distribution reflecting ongoing trends in digital transformation, data sovereignty concerns, and strategic investments. While the global hyperscalers continue to command significant portions of the market, regional providers are carving out niches by focusing on specialized services, regulatory compliance, and localized support, indicating a maturing and increasingly segmented ecosystem.

The overarching trend for 2024 sees the major global cloud infrastructure providers maintaining their dominant positions. Amazon Web Services (AWS), Microsoft Azure, and Google Cloud Platform (GCP) collectively represent a substantial majority of the European market share. Their extensive portfolios, encompassing Infrastructure as a Service (IaaS), Platform as a Service (PaaS), and Software as a Service (SaaS), coupled with their robust global networks and continuous innovation, make them the default choice for many large enterprises and rapidly scaling startups. AWS, historically a frontrunner, continues to leverage its vast service offerings and mature ecosystem to retain a leading edge. Microsoft Azure, propelled by its strong enterprise relationships and hybrid cloud capabilities, has seen consistent growth, particularly in sectors where Microsoft’s software suite is already deeply embedded. Google Cloud, while a later entrant to the top tier, is making significant strides, especially in areas like data analytics, artificial intelligence, and machine learning, attracting organizations looking for cutting-edge technological solutions.

However, the narrative in Europe is not solely defined by these global behemoths. A significant undercurrent of growth and strategic importance is being generated by European cloud providers. These companies, often referred to as "sovereign cloud" or "regional cloud" providers, are increasingly attracting attention from businesses and public sector organizations prioritizing data localization, regulatory compliance, and enhanced control over their digital assets. Concerns surrounding data privacy, particularly in light of regulations like the General Data Protection Regulation (GDPR) and the Schrems II ruling, have amplified the demand for cloud services that guarantee data processing within the European Union’s geographical borders, under European jurisdiction.

Companies such as OVHcloud, a French provider, have positioned themselves as strong contenders by emphasizing their commitment to data sovereignty and offering a comprehensive suite of cloud services, from bare metal servers to public and private cloud solutions. Their transparent pricing and focus on sustainability have also resonated with a growing segment of the market. Similarly, Deutsche Telekom’s T-Systems, Orange Business Services, and other national telecommunications and IT service providers are actively developing and marketing their cloud offerings, often leveraging partnerships with global players for specific technologies while maintaining a strong local presence and understanding of regional business needs.

The market share dynamics are further influenced by the specific sub-segments of the cloud market. In the IaaS and PaaS segments, where infrastructure and platform services are offered, the hyperscalers generally hold the largest shares due to the sheer scale and breadth of their offerings. However, in the burgeoning PaaS and specialized SaaS categories, the competitive landscape becomes more diverse. European providers are finding success in areas like regulated industry clouds (e.g., for healthcare or finance), secure collaboration platforms, and tailored data analytics solutions that meet specific national or regional requirements.

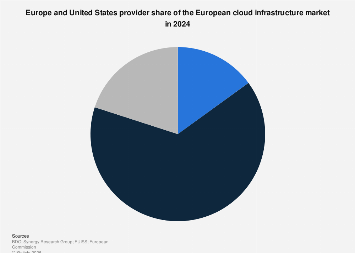

Statistics from market research firms for 2024 indicate that while the top three global providers are projected to collectively hold over 60% of the total European cloud infrastructure market, the remaining share is fiercely contested. This remaining segment, valued in the tens of billions of euros annually, represents a substantial opportunity for regional players. Furthermore, the growth rate of these regional providers, particularly those focusing on sovereign solutions, often outpaces that of the larger, more mature global players in specific European markets. This suggests a strategic shift where enterprises are adopting multi-cloud or hybrid cloud strategies, not just for resilience or cost optimization, but also to meet specific data governance and compliance mandates.

The economic impact of this evolving cloud market in Europe is profound. Increased adoption of cloud services fuels innovation, drives efficiency for businesses, and supports the growth of the digital economy. For European cloud providers, success translates into job creation, technological development within the EU, and a stronger digital sovereignty. The investment in cloud infrastructure also has a multiplier effect, supporting the development of new applications and services that rely on scalable and accessible computing power. The European Commission’s digital decade targets, which aim to increase the EU’s cloud computing capacity and promote the development of trusted cloud services, further underscore the strategic importance of this sector for the continent’s economic future.

Expert insights suggest that the trend towards data localization and regulatory compliance will continue to shape the European cloud market. This will likely lead to further consolidation and specialization among regional providers, as well as increased partnerships between European entities and global hyperscalers. The ability to offer compliant, secure, and performant cloud solutions tailored to the specific needs of European businesses and governments will be a key differentiator. Moreover, the ongoing development of edge computing and specialized cloud services for areas like AI and IoT will create new battlegrounds for market share.

The competitive advantage for European providers often lies in their agility, deeper understanding of local regulatory frameworks, and the ability to offer highly personalized customer support. While global providers may offer economies of scale and a wider array of services, the nuanced requirements of European data protection laws and specific industry regulations can be better addressed by providers with a strong regional focus. This has led to the emergence of various "sovereign cloud" initiatives, often supported by governments, aimed at fostering a secure and independent European cloud infrastructure.

Looking ahead, the European cloud market is poised for continued growth and transformation. The interplay between global hyperscalers and increasingly sophisticated regional providers will drive innovation and offer businesses a wider range of choices. The emphasis on data sovereignty, security, and compliance will remain a central theme, shaping investment decisions and market dynamics. The success of European cloud providers will be crucial in ensuring the continent’s digital autonomy and fostering a competitive digital economy that aligns with its unique regulatory and societal values. The market share figures for 2024, while showing the continued strength of global players, also highlight the growing significance and potential of European alternatives, signaling a more diverse and resilient future for the continent’s cloud landscape.