The intricate tapestry of global commerce is profoundly shaped by China’s vast economic engine, with its bilateral trade balances serving as critical indicators of international economic relationships and shifting geopolitical dynamics. As of early 2024, a nuanced examination of these balances reveals a complex interplay of factors, from robust export performance in key sectors to evolving import demands influenced by domestic policy and global supply chain realignments. Understanding these country-specific trade figures offers invaluable insights into the health of individual economies, the competitiveness of various industries, and the broader trajectory of international trade flows.

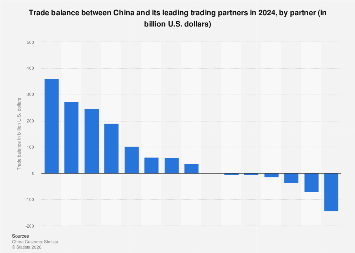

China’s persistent trade surpluses with a significant number of its trading partners underscore its enduring manufacturing prowess and its central role in global supply chains. For instance, its trade relationship with the United States, historically a focal point of trade discussions, continues to exhibit a substantial imbalance, although the precise figures are subject to ongoing adjustments influenced by tariffs, trade policies, and shifts in consumer demand. In 2023, while official data indicated a slight contraction in the overall trade volume between the two nations, China’s surplus remained a defining characteristic. Projections for 2024 suggest a continuation of this trend, albeit with potential moderations as both countries navigate economic headwinds and strategic trade adjustments. The composition of this trade is also crucial; while the U.S. imports a wide array of consumer goods from China, it exports agricultural products, aircraft, and technology components, creating a multifaceted economic interdependence.

Similarly, China’s trade balance with the European Union presents a picture of significant surplus for Beijing. The EU, a major market for Chinese manufactured goods ranging from electronics and textiles to machinery, consistently imports more than it exports to China. This imbalance, while a source of economic benefit for China, also fuels discussions within the EU regarding industrial competitiveness, the need for diversified sourcing, and the promotion of domestic manufacturing. As the EU grapples with inflation and supply chain vulnerabilities, there is a growing impetus to re-evaluate trade strategies, potentially leading to a more balanced, albeit still substantial, trade flow with China in the coming year. The "Made in China 2025" initiative, aimed at upgrading China’s manufacturing capabilities, further complicates this dynamic, suggesting a future where China may compete more directly in higher-value sectors traditionally dominated by European nations.

Beyond these major economic blocs, China’s trade relationships with its Asian neighbors present a more varied tableau. With countries like South Korea and Japan, China often maintains a trade surplus, driven by demand for its finished products and its role as a regional manufacturing hub. However, these relationships are also characterized by significant intra-industry trade, particularly in the electronics and automotive sectors, where components and finished goods flow in both directions. The dynamics with Southeast Asian nations, such as Vietnam and Thailand, are particularly noteworthy. While China is a major trading partner for many of these countries, the balance can fluctuate. Some nations, like Vietnam, have seen their exports to China increase significantly, narrowing the trade gap, as they benefit from their own manufacturing growth and reconfigured supply chains. Others may continue to exhibit a more pronounced surplus in favor of China, reflecting their reliance on Chinese intermediate goods and capital equipment.

The economic impact of these bilateral trade balances extends far beyond mere accounting figures. For China, sustained trade surpluses contribute to its foreign exchange reserves, provide capital for domestic investment, and fuel economic growth. However, they also invite scrutiny and potential trade friction from partners concerned about market access, intellectual property rights, and currency valuations. For deficit countries, persistent trade imbalances can strain national budgets, lead to job losses in import-competing sectors, and create vulnerabilities in their balance of payments. This is why many nations are actively seeking to diversify their trading partners and strengthen their domestic industries to reduce over-reliance on any single economy.

Statistics from various international bodies and economic research firms consistently highlight these trends. For instance, reports indicate that China’s total trade surplus in goods for 2023 reached a record high, underscoring the resilience of its export sector despite global economic slowdowns. This surplus was largely driven by continued strong demand for Chinese manufactured goods, particularly in categories such as electrical machinery, vehicles, and textiles. Looking ahead to 2024, while some economists anticipate a slight moderation in the growth rate of Chinese exports due to softening global demand and increased geopolitical uncertainties, the overall trade surplus is still expected to remain robust.

The composition of China’s imports also offers a window into its evolving economic priorities. While the country continues to import raw materials and components essential for its manufacturing base, there is a discernible shift towards higher-value imports, including advanced machinery, specialized chemicals, and certain consumer goods, reflecting a growing middle class and a desire for technological advancement. This diversification of import demand can, in turn, create new export opportunities for trading partners capable of meeting these specific needs.

Global comparisons further contextualize China’s trade position. While China’s trade volume and surplus are immense, other major economies like Germany and Japan also maintain significant trade surpluses, albeit on a smaller scale and with different trading partners. The United States, conversely, typically runs a substantial trade deficit, highlighting a different economic model centered on consumption and services. Understanding these comparative positions is crucial for comprehending the global distribution of economic power and the interconnectedness of national economies.

The role of international organizations like the World Trade Organization (WTO) and the International Monetary Fund (IMF) remains critical in monitoring these trade flows, providing data, and fostering dialogue to address trade imbalances and disputes. As China’s economic influence continues to grow, its bilateral trade relationships will remain a central focus for policymakers, businesses, and analysts worldwide, shaping the contours of global economic integration and competition for years to come. The data emerging in 2024 will offer crucial insights into how these complex dynamics are evolving in response to global economic shifts, technological advancements, and geopolitical realignments.